The Dynamics of Market Making: The Case of Stablecoins

Exploring liquidity, arbitrage, risk management, and the fragile balance of trust that keeps stablecoins' pegs intact.

Stablecoins Market making is one of the most difficult and poorly understood aspects of decentralized finance, ostensibly because stablecoins neither promise moonshots, nor dominate social feeds with wild charts. Nor do they spark philosophical debates about the future of money. However, beneath that serene exterior, there is an increasingly complex mechanism - known as market making - that keeps stablecoins revolving around their official peg.

To make the expectation of stability work in a nascent and highly turbulent market, It takes ongoing effort, resources and organization that relentlessly help keep all faces of any stablecoin together around the clock. While nobody notices when everything is operating smoothly, the shockwaves spread quickly and widely throughout the cryptocurrency ecosystem when it doesn’t. Understanding how market making works in stablecoins is fundamental. It clarifies the reasons behind pegs' holding, wobbling, and occasionally complete failure. In cryptocurrency, stability is not given, for it is deliberately constructed, protected, and sometimes lost.

What Makes Stablecoin Market Making Different

Market making means providing continuous buy and sell prices so markets can function smoothly. In volatile assets, market makers are paid to take price risk. They step in when others won’t, and they profit from uncertainty.

Stablecoins flip that model on its head.

In stablecoin market marking, not only the goal is the determine the direction of pricing as it is the case with any market making, market markers also need to go beyond that point, to ensure that pricing doesn't move anyplace.

That single constraint changes everything particularly because:

- Profit margins are extremely thin

- Inventory risk is one-sided

- Speed and execution matter more than prediction

- Trust in redemption matters more than charts

Stablecoin market making makes lives in the uncomfortable space between cold mechanics and raw human emotion. When the market assumes a stablecoin to be trading at one ounce of gold, very few people think about what has to happen behind the scenes to keep it there.

In a role defined by asymmetric risk and invisible success, market makers don’t get credit for doing their job well, they only get noticed when something breaks.

The Main Goals of Market Makers for Stablecoins

Market makers and liquidity providers in stablecoin markets operate under much tighter constraints than those trading equities or more volatile crypto assets. On the surface, their role may seem limited—but the consequences of getting it wrong are anything but small. Even minor breakdowns can shake confidence in the peg and ripple through the broader system.

In practice, stablecoin market makers are expected to:

- Keep bid–ask spreads extremely tight around the peg, so prices remain steady and predictable in day-to-day trading.

- Respond quickly to short-term supply and demand imbalances, smoothing out fluctuations without adding unnecessary volatility.

- Support minting and redemptions in an orderly way, allowing supply to adjust without disrupting secondary markets.

- Hold the line during periods of stress, helping prevent panic-driven feedback loops and keeping markets functioning when confidence is fragile.

When everything goes according to plan, stablecoins basically disappear. They become dull—in the greatest sense of the word—quietly doing their role as reliable units of account and exchange. When it doesn’t work, stability disappears faster than most people expect.

What makes this difficult is that market markers’ goals often conflict with basic market making principle essentially because:

- Tight spreads mean low profits.

- Absorbing imbalances means carrying risk.

- Supporting redemptions requires capital precisely when conditions are worst.

Market makers constantly have to decide which objective matters most in the moment, often with incomplete information and very little time.

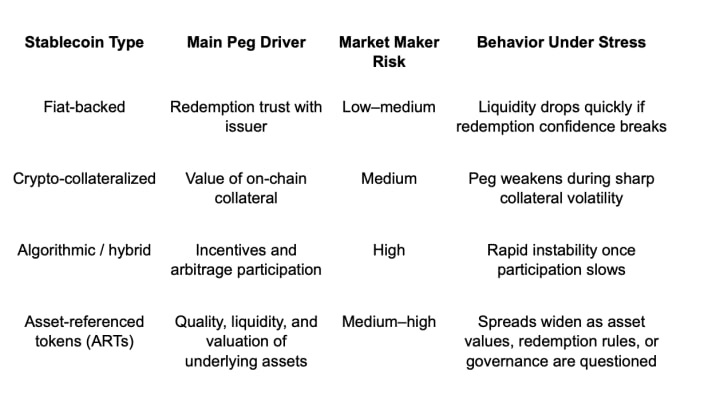

Types of Stablecoins and Why They Matter for Market Making

Stablecoins and the methods used to maintain their liquidity differ from one another.

Fiat-backed stablecoins

These are backed by off-chain reserves held by centralized issuers. From the standpoint of market-making:

- Trust in redemptions is a major factor in peg strength.

- Under typical circumstances, spreads remain narrow.

- If confidence wanes, liquidity swiftly disappears.

In this case, market makers are essentially placing bets on the issuer's reliability. As long as redemptions are smooth, liquidity is deep. Spreads increase and depth thins almost immediately when redemption is questioned, even for a short while.

Stablecoins with cryptocurrency collateral

Over-collateralized cryptocurrency assets secured by smart contracts serve as their backing.

Key characteristics:

- Peg stability is tied to collateral volatility

- Risk modeling is more complex

- Market makers must track underlying crypto health

Even if redemptions aren’t happening, sharp moves in collateral prices can shake confidence. Market makers aren’t just watching the stablecoin — they’re watching the entire collateral ecosystem underneath it.

Algorithmic and hybrid stablecoins

These rely on incentives, arbitrage behavior, and partial collateralization.

From a liquidity standpoint:

- Peg defense depends heavily on active participation

- Sentiment matters more than balance sheets

- Stress events escalate quickly

Here, market making becomes a bet on continued engagement. Once participants step back, stability can unravel faster than most models anticipate.

Asset-referenced tokens (ARTs)

These tokens are backed by a mix of real-world assets such as commodities, bonds, or other financial instruments, instead of relying on a single currency or crypto collateral.

From a market-making perspective:

- Peg stability comes down to asset quality and how often valuations are updated

- Pricing isn’t as clean or intuitive as with fiat-backed coins

- Liquidity depends heavily on clear governance and consistent disclosure

In calm markets, spreads tend to stay fairly steady. Under stress, though, questions around asset values, liquidity, or redemption rules surface quickly, and spreads widen. Market makers aren’t just trading the token — they’re pricing trust in the structure behind it.

Stablecoin Types vs Market-Making Risk

How Market Makers Defend the Peg in Practice

Stablecoin pegs don’t hold themselves, for they are maintained through constant, coordinated action across multiple venues.

Common tactics include:

- Layered buy and sell orders around the peg

- Arbitraging price differences across exchanges

- Rotating liquidity between stablecoins

- Minting or redeeming when price deviations allow

When a stablecoin trades below its peg, market makers buy and expect reversion. When it trades above, they sell into demand. The mechanics are simple, however the execution is not.

These actions happen across time zones, chains, and market structures. Peg defense isn’t a single trade, it’s an ongoing posture that has to adapt continuously as order flow changes.

Arbitrage: The Glue Holding Stablecoins Together

Arbitrage is what quietly keeps stablecoins honest. Without it, pegs drift and spread widen almost immediately.

Arbitrageurs operate between:

- Centralized exchanges

- Decentralized exchanges

- Issuer redemption mechanism

- Bridges that span chains

Despite having very little margins, arbitrageurs’ operations have a huge impact on the market outcome. The success of arbitrageurs is contingency on redemptions being available, costs being predictable, settlement being quick, and risk kept under control at every step of the way. Arbitrage doesn't "fail" when certain circumstances vanish; rather, it becomes unprofitable. Instability is not the result of that lack, it serves as a warning.

Fragmentation of Liquidity: The Undiscovered Flaw

Liquidity for stablecoins is dispersed between protocols, exchanges, and chains, resulting in blind spots.

A stablecoin can look liquid on paper while being unusable in practice.

This leads to:

- Price discrepancies across venues

- Slower peg recovery

- Higher slippage for large trades

- Conflicting confidence signals

Market makers must constantly rebalance across ecosystems. During calm markets, this is manageable. During stress, it becomes extremely difficult — and delays feed panic.

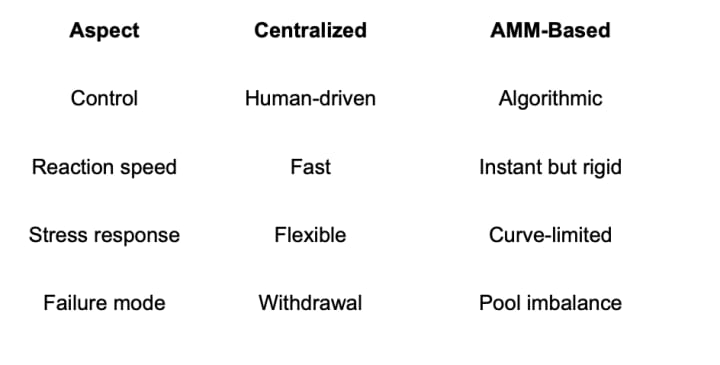

Decentralized Market Making and AMMs

Automated market makers now play a major role in stablecoin liquidity, especially on decentralized exchanges.

Stablecoin pools behave very differently from volatile pairs:

- Impermanent loss is usually low

- Capital efficiency is high near the peg

- Imbalances grow quickly during redemptions

Stable-swap curves are designed for calm conditions, however when fear takes over, even the best curves can’t prevent pools from being drained.

Centralized vs Decentralized Market Making

The Psychological Layer No Model Can Remove

No matter how sophisticated the design, stablecoins ultimately rest on belief.

Math, collateral ratios, and liquidity models matter — but they all sit on top of human confidence, and confidence can vanish faster than any on-chain metric can react.

Behavior changes, the very moment traders feel something is wrong. They stop asking whether a stablecoin is technically solvent and start asking whether they’ll be the last one out. At that point, logic gives way to instinct.

History shows the same pattern repeatedly where peg’s breaks tend to accelerate not because reserves are suddenly gone, but because perception shifts. Market makers, who are usually comfortable absorbing small deviations, begin to reduce exposure, when spread widen. That visible drop in liquidity becomes proof, in traders’ minds, that something must be wrong.

Liquidity often disappears before insolvency is ever confirmed.

This creates a reflexive loop that no spreadsheet can fully model: fear causes liquidity to retreat, and retreating liquidity creates more fear. Once this loop starts, even healthy systems can come under severe pressure.

Stablecoins promise certainty in an uncertain market. When that promise is questioned — even briefly — the emotional reaction is often stronger than in more volatile assets. Ironically, what makes stablecoins useful is also what makes them fragile.

Thin Margins and Heavy Capital Requirements

From the outside, stablecoin market making looks safe. After all, the price barely moves, but that appearance is misleading.

In reality, this is a low-margin, high-responsibility business. Profits are measured in basis points, not percentages. It is not audacious risk-taking that leads to success, but volume, scalability, and perfect execution.

Even modest profits need market makers to invest large sums of money. They rely on tight spreads, high turnover, and precise inventory management. Any mistake — a delayed hedge, a stuck transaction or an unexpected debt — can undo months of steady gains.

And then there’s tail risk.

A single, sharp loss of confidence can trigger conditions where exits disappear and spreads explode. In those moments, the same stability that normally limits downside suddenly offers no protection at all.

This is why stablecoin market making tends to be dominated by large, well-capitalized firms and protocols. Smaller players simply can’t afford the operational complexity or the asymmetric downside. In stablecoins, boring profits come with very real existential risk.

When Stablecoins Markets Get Stressed

Every stablecoin system looks robust in calm conditions. The real test comes during stress.

These moments rarely unfold neatly, instead, several problems tend to appear at once. Redemption requests surge, blockchains become congested, transaction fees spike and arbitrage windows close more slowly than models assume.

In order to safeguard themselves, centralized exchanges may sometimes halt withdrawals, cutting off important channels for liquidity. Market makers start to back off as risk increases and market conditions become more uncertain, reducing depth and amplifying volatility.

What’s dangerous is that none of this requires a fundamental failure.

Often, stress is triggered by uncertainty rather than fact. A rumor, a sudden market crash, or a broader macro shock can be enough to start the process. Once it begins, the system is tested not just on its design, but on its ability to function under pressure and time constraints.

In many historical cases, the first few minutes matter the most. If liquidity holds and communication is clear, confidence can return quickly. If not, small cracks can grow into structural breaks.

Stress events are not rare edge cases. They are the moments stablecoin systems should be designed for — because they are the moments that define credibility.

Lessons from the Failures of Stablecoins

Every stablecoin failure, whether whole or partial, leaves a distinct set of lessons in its wake. The problem is not that these lessons are unknown — it is that they are often ignored during good times.

One of the most common mistakes is relying too heavily on incentives. Many designs assume that arbitrageurs will always act rationally and immediately. In reality, arbitrage dries up when risk feels unbounded or settlement becomes uncertain.

Another recurring issue is liquidity concentration. When too much liquidity sits on a single chain, exchange, or pool, stress in that location can ripple outward. Diversification isn’t just a risk-management concept — it’s a survival requirement.

Collateral also needs ongoing care. Although it helps, over-collateralization is not a guarantee. Rapid price fluctuations have the ability to surpass even conservative buffers if systems are not continuously checked and adjusted. Above all, assurance is not as important as transparency.

Most significantly, transparency is more vital than assurance. Markets can tolerate bad news far better than silence. When users don’t understand reserves, redemption mechanics, or decision-making processes, fear fills the gap.

The core lesson is simple: stablecoins don’t fail only because of flawed math. They fail when trust erodes and liquidity retreats at the same time.

What Sustainable Stablecoin Market Making Really Looks Like

A stablecoin is not maintained by a single process. Combining numerous tiny, diligent practices results in sustainability.

Widespread distribution of liquidity is required, including chains, decentralized pools, and centralized exchanges. No single venue should ever become a critical point of failure. Liquidity also needs to be actively balanced, not just deployed and forgotten.

Reserves must be genuinely redemption-ready. It’s not enough to be solvent on paper. During stress, speed matters as much as size.

Applying risk management in layers yields the best results. Routine security procedures can be handled by automated technology, but unexpected circumstances require human judgment. Circuit breakers, limits, and alarms are important, but professional monitoring is what prevents odd circumstances from becoming major issues. Equally crucial—and occasionally disregarded—is communication. Even quick, timely updates can be quite helpful in preserving confidence and morale during trying circumstances. Panic is fueled by supposition, which is encouraged by silence.

The goal of arbitrage should be to minimize friction. Low fees, predictable settlement, and efficient routing keep the peg healthy without constant intervention.

About the Creator

Mark Arthur

Keynote speaker, author, serial entrepreneur and digital lifestyle evangelist working at the intersection of blockchain and artificial intelligence.

Keep reading

More stories from Mark Arthur and writers in 01 and other communities.

Mainstream Media Persistent Crypto Criticism: Enough is Enough

Even though cryptocurrencies have been making headlines for almost ten years now, the way they are covered is still way to shallow for something that has grown exponentially large and complex. The word crypto is generically mentioned everywhere, in market reports, on cable news panels, in push notifications, and in political debates. However the conversation rarely moves past the surface.

By Mark Arthur8 days ago in 01

Enhancing Agile Software Development in the Trading Industry – A Comprehensive Guide

Financial markets move fast. Software teams don’t always. That gap is where problems begin. In trading, milliseconds matter. A delayed execution, a system freeze during high volatility, or a compliance oversight can cost more than just money — it can cost trust. And yet, many trading platforms are still built using development models that weren’t designed for this level of speed and complexity.

By alan michaelabout 10 hours ago in 01

Comments

There are no comments for this story

Be the first to respond and start the conversation.