Asia Pacific Pharmaceutical Drug Delivery Market Poised to Reach US$687.9 Million by 2031

Strategic Investments in Injectable Systems, Self-Administration Devices, and Digital Health Integration Drive 7.5% CAGR Across China, Japan, India, and Southeast Asia

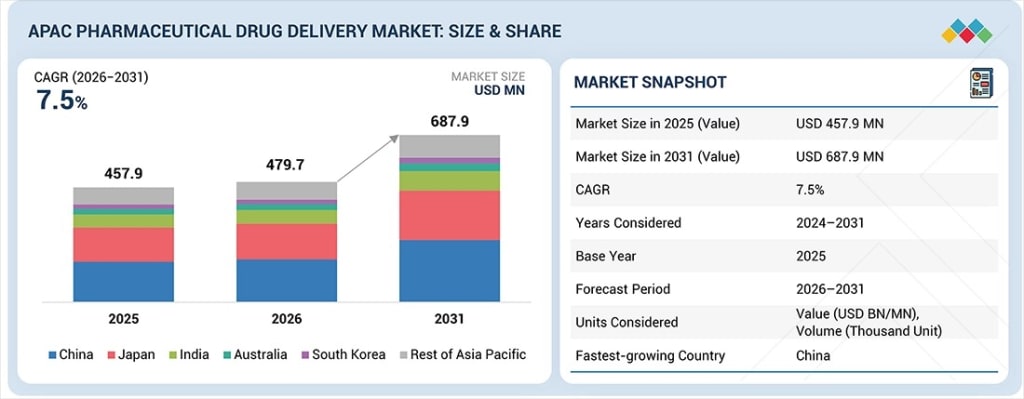

The Asia Pacific pharmaceutical drug delivery market is experiencing transformative growth, advancing from US$479.7 million in 2026 to a projected US$687.9 million by 2031, representing a robust compound annual growth rate (CAGR) of 7.5% throughout the forecast period. This expansion—up from US$457.9 million in 2025—reflects fundamental shifts in regional healthcare infrastructure, disease management strategies, and therapeutic delivery innovation that C-suite executives and strategic decision-makers must understand to capitalize on emerging opportunities.

Download PDF Brochure of Asia Pacific Pharmaceutical Drug Delivery Market

What is driving this regional market acceleration? The convergence of four strategic factors positions APAC as a critical pharmaceutical delivery hub: escalating chronic disease prevalence requiring sophisticated delivery mechanisms, accelerating adoption of biologics and biosimilars demanding specialized administration routes, breakthrough advancements in connected delivery technologies, and expanding regional manufacturing capabilities that are reshaping global supply chains.

Why does this matter now for pharmaceutical and healthcare executives? The market dynamics underpinning this growth directly impact strategic planning across drug development, commercial partnerships, regulatory compliance, and digital health investments. Organizations that fail to align their portfolios with injectable delivery systems, patient-centric self-administration solutions, and digitally-enabled devices risk competitive disadvantage in the world's fastest-growing healthcare market.

Strategic Market Intelligence: Country, Delivery Route, Application, and Facility Insights

Where is the highest growth materializing? China emerges as the dominant growth engine, projected to achieve a 7.8% CAGR during the forecast period—the highest rate across all APAC markets. This leadership reflects substantial government healthcare investments, aggressive biologics manufacturing expansion, and comprehensive cancer care infrastructure development across tier-one through tier-three cities.

How are delivery technologies capturing market share? Injectable drug delivery systems command the largest market segment in 2025, driven by intensifying demand for biologics, biosimilars, vaccine programs, and chronic disease therapies requiring parenteral administration. The proliferation of pre-filled syringes, auto-injectors, infusion devices, and next-generation wearable injectors underscores the market's evolution toward patient convenience and treatment adherence optimization.

Which therapeutic applications demonstrate the strongest momentum? Cancer treatment applications are projected to experience the highest growth rate from 2026 to 2031, propelled by surging oncology incidence across China, India, Japan, South Korea, and Southeast Asia. The expanding adoption of targeted therapies, immunotherapy, and biologics—all requiring sophisticated delivery platforms—creates substantial opportunities for pharmaceutical companies and medical device manufacturers specializing in precision oncology solutions.

Who are the primary adopters of these delivery technologies? Hospitals maintain the largest market share in 2025 within the facility-of-use segment, reflecting APAC's continued reliance on hospital-based administration of injectable therapies, infusion treatments, and cancer care protocols. Major medical centers across China, Japan, and India are simultaneously expanding capacity and upgrading to advanced delivery systems, particularly for high-risk and biologics-based therapies requiring clinical oversight.

Competitive Landscape: Market Leaders and Disruptive Innovators

Who leads the competitive landscape? Terumo Corporation and Pfizer Inc. dominate the APAC pharmaceutical drug delivery market through complementary strategic advantages. Terumo leverages advanced delivery innovations, extensive regional manufacturing presence, and long-standing partnerships with Asian pharmaceutical companies. Pfizer strengthens its position through specialized formulations, mRNA delivery platform expertise, and nanoparticle-based technologies that address emerging biologics requirements.

Which emerging players are reshaping market dynamics? Regional startups including Daewoong Therapeutics (South Korea), Nusantics (Indonesia), and ACM Biolabs (Singapore) are gaining strategic prominence through innovative delivery platforms and next-generation technologies specifically designed for APAC patient populations and healthcare systems. These organizations represent potential partnership or acquisition targets for established pharmaceutical companies seeking accelerated regional market entry.

Established pharmaceutical and medical device leaders operating in this ecosystem include Johnson & Johnson Services, Becton Dickinson and Company, Merck & Co., B. Braun, Gerresheimer AG, Cipla, Eli Lilly and Company, Novartis, Biogen, Baxter International, West Pharmaceutical Services, Sun Pharmaceutical Industries, and GlaxoSmithKline—each bringing differentiated capabilities across oral, injectable, transdermal, and specialty delivery technologies.

Market Dynamics: Drivers, Opportunities, Restraints, and Strategic Challenges

What fundamental drivers are propelling market expansion? Two primary forces accelerate adoption: the rising prevalence of chronic diseases including diabetes, cardiovascular conditions, respiratory disorders, and cancer; and the increasing integration of connected, patient-operated self-administration devices that reduce healthcare system burden while improving treatment adherence and patient outcomes.

Where do the most significant opportunities exist? Growing demand for wearable injectors and home-care delivery solutions represents a transformative opportunity as healthcare decentralizes across the APAC region. Government investments in digital health infrastructure, improved reimbursement frameworks in mature economies, and the imperative to reduce hospital overcrowding create favorable conditions for companies developing patient-centric, digitally-enabled delivery platforms.

What obstacles constrain market acceleration? Wide disparities in regulatory maturity and approval timelines across APAC countries create significant operational challenges. While developed markets such as Japan, Singapore, and Australia maintain efficient regulatory frameworks, emerging economies including Indonesia, Vietnam, and the Philippines exhibit limited regulatory capacity and inconsistent standards—extending product launch timelines and complicating multi-country commercialization strategies.

How does competitive pressure impact profitability? Intense competition from low-cost local manufacturers in China, India, and Southeast Asia poses substantial margin pressure, particularly for standard delivery systems including syringes, infusion sets, and basic administration devices. Regional competitors leverage economies of scale and lower operational costs to offer highly competitive pricing that global players struggle to match without sacrificing quality or innovation investments.

Technology Disruption and Customer Impact: The Transformation of Drug Delivery

What technological disruptions are reshaping patient care? The APAC pharmaceutical delivery market is undergoing rapid transformation driven by biologics and biosimilars proliferation. IoT-enabled devices, microneedle patches, nanoparticle delivery systems, and smart inhalers are fundamentally changing treatment paradigms by enabling precise dosing, real-time monitoring, and enhanced patient engagement.

Why are vendors accelerating automation and compliance investments? Ascending demand for patient self-administration capabilities, pressure to scale production rapidly, and stringent government regulatory standards compel vendors to develop increasingly automated, compliant, and user-friendly drug delivery solutions. This evolution addresses both patient preference for home-based care and healthcare systems' capacity constraints.

Ecosystem Collaboration: The Foundation for Sustainable Market Growth

Who comprises the pharmaceutical drug delivery ecosystem? Strategic collaboration among pharmaceutical manufacturers, medical device companies, contract development and manufacturing organizations (CDMOs), digital health platforms, hospitals, regulatory bodies, and innovative startups forms the integrated ecosystem driving APAC market advancement. This collaborative framework accelerates technology adoption, enhances patient access, expands localized manufacturing for injectables and biologics, and facilitates next-generation delivery system development.

How do ecosystem partnerships strengthen competitive positioning? Global pharmaceutical companies increasingly partner with APAC CDMOs to leverage regional manufacturing expertise, optimize supply chain efficiency, and accelerate time-to-market for complex biologics and combination drug-device products. These strategic alliances simultaneously reduce costs and improve responsiveness to local market requirements.

Market Segmentation: Strategic Implications Across Routes, Applications, and Facilities

The APAC pharmaceutical drug delivery market encompasses diverse administration routes—oral, injectable, topical, ocular, nasal, implantable, and transmucosal—each addressing specific therapeutic requirements and patient populations. Injectable delivery maintains dominance due to biologics growth, chronic disease management needs, and advancing hospital infrastructure.

Therapeutic applications span infectious diseases, cancer, cardiovascular conditions, diabetes, respiratory diseases, central nervous system disorders, autoimmune diseases, and specialized treatments. The cancer segment's projected leadership reflects both disease burden escalation and therapeutic innovation requiring sophisticated delivery platforms.

Facility utilization extends across hospitals, ambulatory surgery centers, clinics, home care settings, diagnostic centers, and specialized facilities. While hospitals currently dominate, the strategic shift toward home-based care represents a fundamental market restructuring with implications for product design, reimbursement models, and commercial strategies.

Recent Strategic Developments Shaping Market Evolution

What recent corporate actions signal market direction? Strategic transactions and partnerships demonstrate intensifying competition for APAC market position. In February 2024, AstraZeneca acquired Gracell Biotechnologies to expand advanced cell therapy capabilities and strengthen its China presence—signaling the strategic importance of localized innovation and manufacturing.

In October 2023, Boehringer Ingelheim partnered with Precision Health Research to advance precision healthcare in Singapore, positioning for improved patient outcomes across APAC markets. Bayer's July 2023 collaboration with Peking University accelerated drug discovery and translational research across oncology, cardiometabolic diseases, immunology, and cell and gene therapies in China.

Sanofi's August 2022 agreement with Innovent Biologics to expedite oncology medicine development exemplifies the partnership model global pharmaceutical leaders employ to strengthen commercial footprint and accelerate regional market penetration.

Strategic Implications for C-Suite Decision-Makers

Why should this market command executive attention? The APAC pharmaceutical drug delivery market represents more than incremental growth—it embodies a fundamental restructuring of global pharmaceutical supply chains, therapeutic delivery paradigms, and patient engagement models. The region's 7.5% CAGR substantially exceeds mature market growth rates, while demographic trends, urbanization, improved diagnostics, and government healthcare investments create sustained multi-year tailwinds.

How can organizations capitalize on these opportunities? Strategic success requires balanced investment across multiple dimensions: advanced delivery technology platforms addressing biologics and specialty therapeutics; digital health integration enabling connected devices and real-time patient monitoring; regional manufacturing partnerships optimizing supply chain efficiency and regulatory navigation; and patient-centric design emphasizing self-administration, adherence support, and home-based care compatibility.

Organizations must simultaneously address regulatory complexity through experienced local partnerships, competitive pricing pressure through innovation differentiation rather than cost-matching, and ecosystem collaboration through strategic alliances spanning pharmaceutical manufacturers, device companies, CDMOs, and digital health platforms.

Market Outlook and Investment Priorities

The APAC pharmaceutical drug delivery market's trajectory from US$479.7 million in 2026 to US$687.9 million by 2031 creates substantial opportunities for pharmaceutical companies, medical device manufacturers, healthcare investors, and digital health innovators. The market's evolution toward injectable biologics, connected self-administration devices, and home-based care solutions aligns with broader healthcare decentralization trends and value-based care imperatives.

Geographic expansion prioritizing China's 7.8% growth trajectory, therapeutic focus emphasizing cancer and chronic disease applications, and technology investments in wearable injectors, smart delivery platforms, and nanoparticle systems position organizations for sustainable competitive advantage in the world's most dynamic pharmaceutical market.

About the Creator

Keep reading

More stories from Jennifer Reynolds and writers in Futurism and other communities.

Europe In Vitro Diagnostics Market Set to Reach USD 49.49 Billion by 2031

The Europe in vitro diagnostics (IVD) market is entering a decisive growth phase as healthcare systems, policymakers, and life sciences leaders intensify investments in early detection, automation, and precision medicine. Valued at USD 31.43 billion in 2025 and USD 33.83 billion in 2026, the market is projected to expand at a resilient CAGR of 7.9% from 2026 to 2031, reaching USD 49.49 billion by the end of the forecast period.

By Jennifer Reynolds12 days ago in Futurism

Aircraft Seating Market: Premium Economy Expansion, Ergonomic Seating & Growth Outlook

According to IMARC Group's latest research publication, The global aircraft seating market size reached USD 6.3 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 9.7 Billion by 2033, exhibiting a growth rate (CAGR) of 4.69% during 2025-2033.

By James Whitman4 days ago in Futurism

Global Data Center Accelerator Market Poised for Robust Growth, Driven by AI and High-Performance Computing Demand

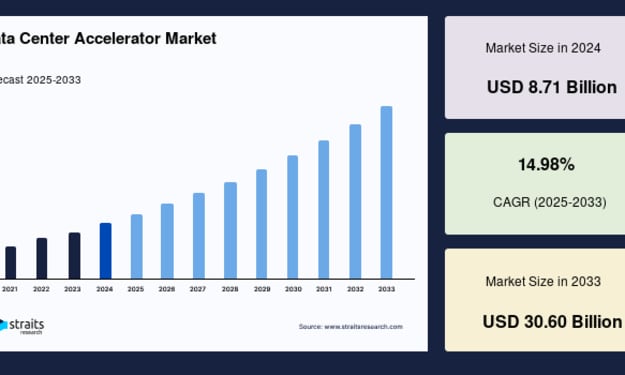

New York, USA – Straits Research, a leading provider of business intelligence and market research, has released its latest report on the Global Data Center Accelerator Market, revealing strong growth prospects driven by the rapid adoption of artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), and cloud-based services. According to the report, the global data center accelerator market size was valued at USD 8.71 billion in 2024 and is projected to reach USD 30.60 billion by 2033, expanding at a compound annual growth rate (CAGR) of 14.98% from 2025 to 2033.

By Sarthak Gandhi3 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.