The Global EV Charging Revolution: Bridging the Gap Between Ambition and Infrastructure

Policy Support, Technological Advancements, and Investment Driving the Future of Electric Mobility Infrastructure

In the early 2010s, the "range anxiety" conversation dominated the electric vehicle (EV) sector. Early adopters lived in fear of being stranded with a dead battery on a lonely highway. Fast forward to the mid-2020s, and the conversation has fundamentally shifted. We no longer worry about how far the car can go—modern EVs easily clear the 300-mile mark. Instead, we have entered the era of "Charging Anxiety."

The Electric Vehicle Charging Station market is currently the most critical bottleneck in the global energy transition. It is no longer just a hardware business; it is a complex intersection of real estate, software, high-voltage electrical engineering, and geopolitical maneuvering. As we look toward 2030, the market is projected to skyrocket, but the path from here to there is fraught with technical and economic hurdles.

1. The Death of the "Wild West" Phase

For the last decade, the EV charging market felt like the Wild West. Drivers had to carry half a dozen different RFIDs and apps to navigate a fragmented landscape of proprietary networks. Hardware was often unreliable, with "broken charger" becoming a common trope on social media.

We are now witnessing the "Great Consolidation." The industry is moving toward standardized protocols. In North America, the massive shift toward the North American Charging Standard (NACS)—originally Tesla’s proprietary plug—has forced every major automaker to pivot. This standardization is the first step toward a "utility" mindset, where charging an EV is as thoughtless and reliable as turning on a light switch.

2. The Power of High-Output: Level 2 vs. DCFC vs. MCS

The market is currently bifurcated into two distinct use cases, with a third on the horizon for heavy industry.

The Residential and Workplace Anchor (Level 2)

Level 2 charging (AC) remains the backbone of the industry. Statistics show that roughly 80% of charging still happens at home or work. The market for "Smart Chargers" is booming here. These aren't just plugs; they are energy management systems that communicate with the grid to charge when prices are lowest and renewable energy production is highest.

The Highway Pulse (DC Fast Charging)

Public fast charging (DCFC) is where the "big oil" transition is happening. Companies like Shell, BP, and TotalEnergies are aggressively acquiring charging startups. They realize that while they might lose revenue on gasoline, they can keep the customer at their "energy hubs." The goal is 150kW to 350kW speeds—fast enough to add 200 miles of range in the time it takes to buy a sandwich and use the restroom.

The Heavy-Duty Frontier (Megawatt Charging)

The next massive growth area is the electrification of Class 8 trucks. Standard DC fast chargers are too slow for a 500kWh truck battery. Enter the Megawatt Charging System (MCS). Capable of delivering over 1,000 kilowatts, these chargers will revolutionize logistics, allowing long-haul truckers to recharge during their mandatory 30-minute rest periods.

3. The "Uptime" Crisis: Why Reliability is the New Currency

The biggest threat to the EV market isn't a lack of chargers, but a lack of working chargers. Studies in major metropolitan areas have shown that at any given time, 20% to 30% of public chargers may be out of commission due to software glitches, payment processing errors, or physical damage.

This has triggered a wave of "Uptime Legislation." Governments are no longer handing out subsidies for simply installing a charger; they are now mandating 97% or 99% uptime. This shift is moving the market away from low-cost hardware manufacturers and toward premium "integrated" operators who offer 24/7 remote monitoring and rapid-response maintenance teams.

4. The Grid Problem: Why "The Last Mile" is Hard

The most significant hidden cost in the EV charging market isn't the charger itself—it's the grid connection. If a developer wants to install ten 350kW chargers at a highway rest stop, they are essentially asking the utility for 3.5 megawatts of power. That is equivalent to the power draw of a small town.

In many places, the local transformers and substations simply aren't built for this. Upgrading this infrastructure can take years and cost millions. To solve this, the market is seeing a surge in Battery-Buffered Charging. By installing a massive stationary battery (BESS) alongside the chargers, the station can "sip" power from the grid 24/7 and then "gulp" it into vehicles at high speeds when they arrive. This mitigates the need for expensive grid upgrades and allows for charging during peak hours without incurring massive "demand charges" from the utility.

5. Charging-as-a-Service (CaaS): The New Business Model

For commercial fleets—think Amazon delivery vans or Hertz rental cars—the upfront cost of installing 500 chargers is prohibitive. This has birthed the "Charging-as-a-Service" model.

Under CaaS, a provider handles the site design, hardware, installation, and energy procurement. The fleet owner pays a flat monthly fee or a price per kWh. This de-risks the transition for businesses, moving the expense from CapEx (Capital Expenditure) to OpEx (Operating Expenditure). We expect CaaS to become the dominant model for the commercial sector over the next five years.

6. Retail Synergy: The "Dwell Time" Economy

Retailers have discovered that EV chargers are "high-value customer magnets." Data indicates that EV drivers tend to have higher-than-average household incomes and spend more time in stores while their cars charge.

Walmart, IKEA, and Target are no longer seeing chargers as an "eco-friendly perk" but as a core foot-traffic driver. By placing chargers at the front of the lot, they increase "dwell time." If a customer knows they have 25 minutes of charging, they are significantly more likely to walk into the store and spend $50. This synergy is creating a secondary revenue stream for the charging market: advertising and retail partnerships.

7. Vehicle-to-Grid (V2G): The EV as a Power Plant

Perhaps the most exciting evolution in the charging market is the shift from "one-way" to "two-way" energy. V2G technology allows the car to send power back to the grid during peak demand.

Imagine a million EVs plugged in during a summer heatwave. Instead of the utility firing up a polluting "peaker" coal plant, it can pull a small amount of energy from each car battery to stabilize the grid. The car owner gets paid for this service. In this scenario, the charging station becomes a bi-directional gateway, and the EV becomes a decentralized power plant.

8. Regional Power Plays: China vs. The World

China currently dominates the charging landscape, boasting more public chargers than the rest of the world combined. Their strategy is top-down and highly integrated.

In contrast, the US and European markets are more fragmented and driven by private investment. However, the US "National Electric Vehicle Infrastructure" (NEVI) program is pumping $5 billion into highway charging, and Europe’s "Alternative Fuels Infrastructure Regulation" (AFIR) is mandating fast chargers every 60km. The race is on to see which region can build a truly seamless continental network first.

9. Conclusion: The Roadmap to 2030

The Electric Vehicle Charging Station market is graduating from its awkward teenage years. The focus is shifting from "quantity" to "quality." The winners of the next decade will be the companies that can solve the reliability issue, integrate battery storage to bypass grid limitations, and create a seamless user interface.

We are building a new global energy network in real-time. It is a monumental task that requires trillions in investment, but the rewards—a decarbonized transport sector and a more resilient, decentralized grid—are worth the effort. For investors, developers, and drivers, the message is clear: the infrastructure is no longer an afterthought; it is the main event.

Key Takeaways for Stakeholders:

For Investors: Look past the hardware manufacturers. The real value is moving toward software-driven energy management and maintenance-heavy operators.

For Retailers: Chargers are the new "free Wi-Fi." If you don't have them, your customers will go to the competitor who does.

For Utilities: EVs are both a threat and an opportunity. Managed charging is essential to prevent grid overload and unlock the potential of V2G.

About the Creator

Rahul Pal

Market research professional with expertise in analyzing trends, consumer behavior, and market dynamics. Skilled in delivering actionable insights to support strategic decision-making and drive business growth across diverse industries.

Carmine Market Insights: Sustainability Concerns, Supply Dynamics & Industry Forecast to 2033

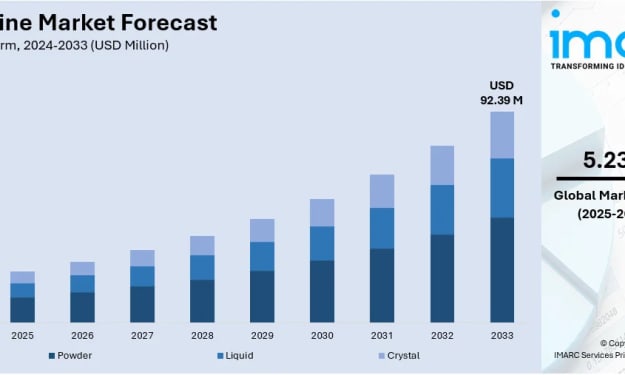

Rising health consciousness, ethical sourcing practices, and preference for natural ingredients are driving carmine market demand, supported by clean-label trends, expanding cosmetics applications, and growing pharmaceutical use. The global carmine market size was valued at USD 57.06 Million in 2024. Looking forward, the market is expected to reach USD 92.39 Million by 2033, exhibiting steady growth.

By Andrew Sullivan2 days ago in Futurism

In-vitro Colorectal Cancer Screening Tests Market Outlook: Early Detection Demand and Growth Opportunities

According to IMARC Group's latest research publication, The global in-vitro colorectal cancer screening tests market size was valued at USD 1,049.22 Million in 2024. The market is projected to reach USD 1,658.67 Million by 2033, exhibiting a CAGR of 4.96% from 2025-2033.

By Michael Richardabout 6 hours ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.