AI in Financial Risk Management: Future Strategies (2026)

Explore how AI in financial risk management transforms banking with automated compliance and fraud detection. Learn more about proactive anomaly detection.

I remember sitting in a risk committee meeting back in 2023, watching a poor analyst try to explain why their linear regression model missed a massive credit default. It was painful. Fast forward to 2026, and if you're still relying on spreadsheets and gut feelings, you aren't just behind the curve—you're playing a different sport entirely. The adoption of AI in financial risk management has moved from "nice to have" to "adapt or die."

Real talk: the landscape has shifted violently. We used to worry about whether the AI model was biased. Now? We are worried about whether our AI agents are fast enough to catch the synthetic identity fraud bots attacking our APIs in milliseconds.

The Agentic Shift: It’s Not Just Automation Anymore

Here is why 2026 feels different. We aren't just using predictive AI anymore; we are in the era of agentic AI.

For years, we treated AI like a really smart intern—you give it data, it gives you a report, and you make the decision. But that’s changing. According to a 2026 report from Citizens Bank, a staggering 82% of midsize companies and 95% of Private Equity firms plan to implement agentic AI this year [1].

These aren't just chatbots. These are autonomous agents that can reason, plan, and execute.

"AI is rewriting both sides of the fraud playbook. Bad actors and small-time fraudsters are using it to launch sharper attacks... at the same time, it's also arming firms with smarter defenses." — Michael Cummins, EVP, Citizens Bank [1].

Thing is, these agents don't just flag a suspicious transaction; they freeze it, investigate the geolocation, cross-reference it with the dark web, and draft the Suspicious Activity Report (SAR) before a human analyst has even had their morning coffee. It’s proper brilliant, but it’s also terrifying if your governance isn't sorted.

Why The Old Ways Are Dead

Let me explain. Traditional risk models were reactive. They looked at what happened yesterday to guess what might happen tomorrow.

- Old Way: "This transaction looks weird." (Flagged for manual review 24 hours later).

- 2026 Way: "This transaction matches a synthetic identity pattern used in a coordinated attack 3 seconds ago in Singapore. Blocked."

The speed difference is gnarly. And if you think you can survive without this level of automation, you're dreaming.

Fraud Detection on Steroids

You know what used to drive me crazy? False positives. Blocking a legitimate customer’s card just because they bought a coffee in a different city was the quickest way to lose business.

But wait, the data is finally showing improvements. New verified data from Keyrus indicates that advanced AI systems have reduced false positive rates by up to 60% [3]. That is huge. It means fewer angry phone calls and more actual fraud catching.

Banks are realizing they can't build all this tech in-house. While the giants like JPMorgan might have armies of engineers, regional players often need specific help to integrate these secure interfaces. It reminds me of how niche tech partners operate; for instance, Mobile app development Wisconsin teams are increasingly being tapped by regional fintechs to build secure, biometric-enabled front ends that feed directly into these risk engines Mobile app development Wisconsin.

It’s a smart play. You let the specialized devs handle the interface while your internal teams focus on the risk models.

The Financial Impact

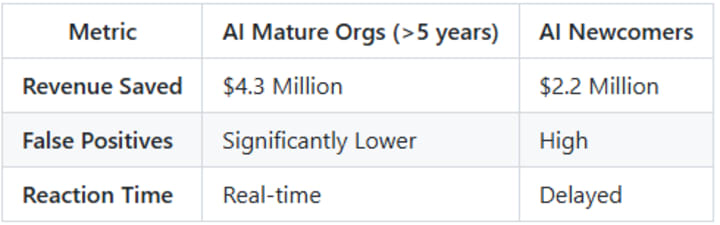

Let's look at the numbers, because money talks. Mastercard’s 2026 report found that organizations using AI for fraud prevention for over five years are saving an average of $4.3 million annually in lost revenue, compared to just $2.2 million for those new to the game [4].

If that doesn't convince your CFO to sign the check, nothing will.

Compliance and The Regulatory Hammer

Speaking of checks, let's talk about the regulators. They aren't sleeping.

The EU AI Act rules for high-risk AI systems fully come into effect in August 2026 [5]. If you are operating in Europe—or even just processing data for European clients—you are fixin' to have a headache if your models aren't compliant.

This is where Generative AI is actually saving our bacon. We are seeing banks use GenAI to digest thousands of pages of new regulations and map them directly to internal controls. It’s no longer a room full of lawyers reading PDFs; it’s an LLM parsing the changes and an AI agent updating the compliance dashboard.

Verified Insight

💡 Lloyds Banking Group (@LBGplc): "Agentic AI isn't just a buzzword; 2026 is the year it moves from promise to practice, shifting finance from automation to autonomous goal-driven systems." [6]

Future Trends: What’s Coming Next?

So, where is this all going? If you reckon we've hit the ceiling, think again.

1.Open Source vs. Proprietary Models There is a massive debate raging right now. Do you trust OpenAI/Google with your risk data, or do you run your own open-source model? Alexandra Mousavizadeh from Evident puts it perfectly:

"Open source models can help banks close the gap with early movers, unlock cost efficiencies and safeguard against vendor lock-in." [2] I expect to see more banks running "small language models" (SLMs) on-premise to handle sensitive risk data without it ever leaving the building.

2. The Rise of "Self-Healing" Risk Models We are seeing early signals of models that detect their own drift. Instead of waiting for a quarterly validation, the AI realizes its predictions are getting worse and automatically retrains itself on the latest market data. It’s hella smart, but it raises massive governance questions. Who is responsible if the model retrains itself into a bias?

3. Quantum Risk Analysis Okay, this is a bit "out there," but with NVIDIA reporting 21% of firms already deploying AI agents [2], the compute power is ramping up. We are inching closer to quantum-inspired algorithms that can run Monte Carlo simulations in seconds rather than hours.

Final Thoughts

Look, the train has left the station. With 65% of financial organizations actively using AI in 2026 (up from 45% last year) [2], sitting on the fence is no longer a strategy. It's a liability.

The winners in 2026 won't be the banks with the most branches; they'll be the ones with the best agents. The ones who can spot a risk before it happens, treat their customers like humans (by not freezing their cards randomly), and navigate the regulatory minefield without exploding.

So, are you going to lead the charge, or are you just fixin' to get left behind?

About the Creator

Keep reading

More stories from Sherry Walker and writers in Geeks and other communities.

Building AI Apps in 2026: The "No-BS" Architecture Guide

I remember back in 2023 when slapping a UI on top of GPT-4 was considered a "startup." Cute, wasn't it? Fast forward to 2026, and that wrapper strategy is dead in the water. If you're still building stateless chatbots that just ping an API and pray for a good response, you aren't building a business. You're building a feature that Apple or Google will ship natively next Tuesday.

By Sherry Walker3 days ago in Geeks

No Other Choice (2025)

It is only February, so other films may well surpass “No Other Choice”, but I think this is the best film I’ve seen so far this year. And that surprises me, because, it is a subtitled film and while I am pretentious enough to choose to watch foreign-language films, I was also very tired and that was an extra commitment from me. But more importantly, let me warn you, this film is gruesome and violent. There were times I had to turn away from the screen to avoid the worst of it (including some self-inflicted dentistry).

By Rachel Robbinsabout 5 hours ago in Geeks

Super Bowl Commercials 2026 Will Reflect a Changing America

Every year, millions of people tune in to the Super Bowl for more than football. They come for the ads. Super Bowl commercials have become shared moments, talked about at work, online, and around dinner tables. By 2026, the world will feel different again. Tastes will shift. Emotions will feel closer to the surface. Brands will still compete for attention, but the way they speak to people will quietly change. Super Bowl commercials 2026 will not just try to be funny or loud. They will try to feel real. This article looks at what these commercials are likely to say about culture, emotion, money, trust, and how people want to feel when they watch the biggest game of the year.

By Muqadas khan3 days ago in Geeks

📢 Raise Your Voice Thread: 02/05/2026

Our “Raise Your Voice Threads” are hosted most alternating Thursdays at 12PM ET to offer creators more avenues to uncover exceptional stories on Vocal. As we are continuously searching for fresh creators and inspiring stories, this thread provides an opportunity to exchange and discuss the stories that have moved and motivated us on Vocal.

By Raise Your Voice by Vocal7 days ago in Resources

Comments

There are no comments for this story

Be the first to respond and start the conversation.