Germany Insurtech Market Report 2025: Resilience Amidst the European VC Funding Winter

The Health and Auto insurance sectors are leading the charge, driven by Germany's Digital Care Act (DVG) and the rise of telematics in vehicle manufacturing.

If you strictly follow the headlines, the European startup scene appears frozen. Venture capital funding has retreated, valuations have reset, and the era of "free money" is officially over. However, headlines often miss the structural reality beneath the surface. In Germany, the continent's largest economy, the insurance technology sector is not just surviving; it is actively evolving.

According to recent data from the IMARC Group, the Germany insurtech market reached a value of USD 728.00 Million in 2024. While current liquidity remains tight, the long-term trajectory is undeniable. Analysts forecast the market to surge to USD 6,513.70 Million by 2033, driven by an aggressive CAGR of 24.50%. This divergence between short-term capital constraints and long-term market expansion suggests that the current "Winter" is actually a maturing phase. It strips away the hype to reveal a resilient, profitable core.

What Does the Data Say About the Actual Size of the Germany Insurtech Market?

The market is far from shrinking; it is projected to grow nine-fold over the next decade due to the digitalization of Germany's massive legacy insurance sector.

To understand the resilience of this sector, one must look at the fundamentals. A growth rate of 24.50% is exceptional for a mature economy like Germany. This figure indicates that the shift toward digital insurance is not a temporary trend but a structural replacement of analog processes.

The jump from USD 728 Million to over USD 6.5 Billion will not be driven by flashy marketing campaigns. Instead, it will be fueled by the "backend revolution." Germany’s insurance industry - one of the oldest in the world - is finally migrating its core systems to the cloud. Consequently, this modernization creates a massive revenue opportunity for insurtechs that provide the infrastructure for automated underwriting, AI-driven claims processing, and digital policy management.

Expert Insight: “The market correction is healthy. It forces companies to focus on unit economics rather than vanity metrics. The survivors of 2025 will be the giants of 2030.”

Why Is the "Funding Winter" Hitting German Insurtechs So Hard?

Investors have shifted their focus from "growth at all costs" to "immediate profitability," causing a sharp decline in early-stage funding rounds while consolidating capital into proven leaders.

The drop in deal volume is real. In 2021, a slide deck and a promise were often enough to raise a Series A. In 2025, however, investors demand positive unit economics. This shift has been painful for B2C "neocarriers" that relied on burning cash to acquire customers.

However, smart capital is still active. A prime example of this resilience is Berlin-based Wefox. Despite the gloomy macroeconomic climate, the company secured a significant €170 million (approx. $184M) financing package in early 2025. This deal sends a clear signal: the funding window is not closed; it is just much more selective. Investors are doubling down on "category winners" that can demonstrate a clear path to profitability, even if it means accepting lower valuations than in previous years.

How Are German Insurtechs Surviving Without Easy Capital?

Smart startups are pivoting from expensive B2C customer acquisition models to B2B "Enabler" strategies, helping legacy insurers digitize rather than competing against them.

The most successful pivot of 2025 has been the move toward "Embedded Insurance." Rather than trying to sell a policy directly to a consumer (which is expensive), insurtechs are integrating their products into the purchase flow of other services. For example, buying travel insurance with a single click while booking a flight, or adding device protection at the checkout of an electronics store.

This B2B2C approach drastically lowers the Customer Acquisition Cost (CAC). Furthermore, many German insurtechs are rebranding as "technological partners." They sell their proprietary AI risk algorithms to traditional giants like Allianz or Munich Re. By becoming indispensable vendors to the incumbents, these startups secure steady, recurring revenue streams that are immune to VC sentiment.

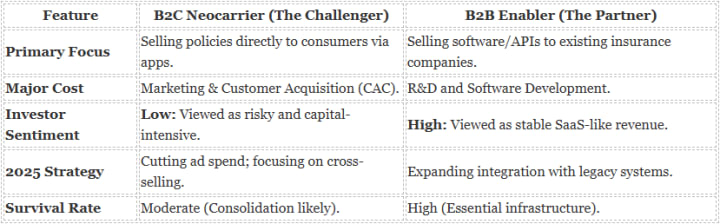

B2C vs. B2B: Which Business Model Is Winning in 2025?

B2B models currently attract more stable investment because they avoid the high marketing costs associated with direct-to-consumer sales.

The "Winter" has clarified which business models are sustainable. Below, we compare how the market views the two primary approaches in the current climate.

Comparison: B2C Neocarriers vs. B2B Enablers

Which Specific Sectors Are Driving the 24.5% CAGR?

The Health and Auto insurance sectors are leading the charge, driven by Germany's Digital Care Act (DVG) and the rise of telematics in vehicle manufacturing.

While the general market is growing, two verticals are outperforming the 24.5% average:

Digital Health & The DVG Effect

Germany’s regulatory environment has become surprisingly progressive. The Digitale Versorgung Gesetz (DVG) allows doctors to prescribe digital health apps. Crucially, statutory health insurance covers these costs. This legislation exploded the market for insurtechs that bridge the gap between patients, apps, and payers. Startups now race to get their applications listed in the DiGA directory, unlocking immediate access to millions of insured patients.

Auto Insurance & Telematics

Germany is an automotive nation. As vehicles become "computers on wheels," the data they generate is transforming auto insurance. Usage-Based Insurance (UBI) - where premiums are based on actual driving behavior rather than statistical demographics - is becoming the standard. Insurtechs that can collect and analyze this telematics data are essential partners for German car manufacturers. They allow for "pay-how-you-drive" models that appeal to younger, safer drivers.

How Does Regulation Impact the German Market?

Strict oversight by BaFin (Federal Financial Supervisory Authority) ensures stability, but it also creates a high barrier to entry that favors established players.

Germany is known for its rigorous bureaucracy. For insurtechs, this is a double-edged sword. On one hand, obtaining a full carrier license from BaFin is a long, expensive process. This difficulty discourages "fly-by-night" operators and increases trust in the system. On the other hand, it forces many startups to operate as Managing General Agents (MGAs), partnering with established insurers to underwrite the actual risk.

Furthermore, compliance with Solvency II regulations remains non-negotiable. Insurtechs that automate compliance reporting - turning a manual, month-long audit into a real-time dashboard - are currently seeing massive demand. Regulatory technology, or "RegTech," is rapidly becoming a sub-sector of its own within the insurtech space.

What Is the Forecast for the German Insurtech Landscape by 2033?

The market will likely consolidate into a hybrid ecosystem valued at over USD 6.5 Billion, where the distinction between "traditional insurer" and "insurtech" disappears.

The IMARC Group's forecast of USD 6,513.70 Million paints a picture of a transformed industry. By 2033, we will likely stop using the word "Insurtech." Technology will be so deeply integrated into every aspect of insurance - from the moment a policy is quoted to the second a claim is paid - that the distinction will be meaningless.

We expect a wave of Mergers and Acquisitions (M&A) over the next three years. Traditional insurers, sitting on cash reserves, will acquire the most promising B2B startups to internalize their tech stacks. Meanwhile, the surviving B2C players will likely merge to achieve the scale necessary to compete with the incumbents.

Conclusion

The "European VC Funding Winter" is real, but it is not a death sentence. For the Germany insurtech market, it is a crucible. The companies that emerge from this period will be leaner, more efficient, and fundamentally more profitable than the "unicorns" of the past decade.

With a projected market size of USD 6.5 Billion and a growth rate of 24.5%, the data suggests that now is not the time to retreat. It is the time to identify the resilient builders who are laying the digital foundation for the next generation of German insurance.

About the Creator

Joey Moore

I'm Joey Moore, a seasoned Research Analyst with 5+ years of experience in market research. Expert in data analysis, strategic planning, and industry insights. Proven track record in delivering actionable reports.

Keep reading

More stories from Joey Moore and writers in Journal and other communities.

Latin America’s Money Engine: Brazil Accounts for 14.92% of the Regional Fintech Investment Share

The financial landscape of Latin America is undergoing a seismic shift. For decades, traditional banking giants held an unshakeable monopoly over the region's economy. Today, that monopoly is dissolving, replaced by agile, digital-first solutions that prioritize accessibility and speed. At the center of this revolution lies a single, powerful engine: Brazil.

By Joey Moore14 days ago in Journal

~ Fired ~

— Ai Intrusion ~ Are you Next ~ Is Ai Evolution after your job? — Few workplaces haven't been affected. Ai is in supermarkets, at doctors' offices, and even monitoring farms. I just can't think of anything this machine is not getting into, can you? For instance: Education ~ Law and Tech jobs will one day have a major influence or be taken over by these inanimate machines, with accuracy and vigor. From mechanics' diagnoses to a wide variety of everyday jobs, including fast food workers, with this input having the ability to cut their unnecessary work hours. I'm certain all of us have been touched by this with our short stories and colorful headings, have you? Even comments are very questionable 'Non-Robot' insertions.

By Jay Kantor17 days ago in Journal

The Role of OpenAI in Business Innovation in 2026

By 2026, artificial intelligence is no longer an experimental add-on inside organizations. It has become infrastructure. Across industries, companies are building workflows, customer journeys, and product strategies around AI systems that generate content, automate analysis, assist decision-making, and accelerate execution. At the center of this shift is OpenAI, whose models and tools are shaping how businesses rethink productivity, creativity, and scale.

By Scott Anderyabout 20 hours ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.