Europe Distributed Control Systems Market Trends & Summary (2025–2033)

How Smart Automation, Industry 4.0, and Energy Transition Are Reshaping Europe’s Industrial Control Landscape

Introduction: A Smarter Backbone for Europe’s Industry

Europe’s industrial sector is in the middle of a profound transformation. From energy and chemicals to food processing and pharmaceuticals, manufacturers are under pressure to become more efficient, more sustainable, and more digitally connected. At the heart of this transformation lies the Distributed Control Systems (DCS) market—an essential technology backbone that enables complex industrial processes to be monitored, controlled, and optimized in real time.

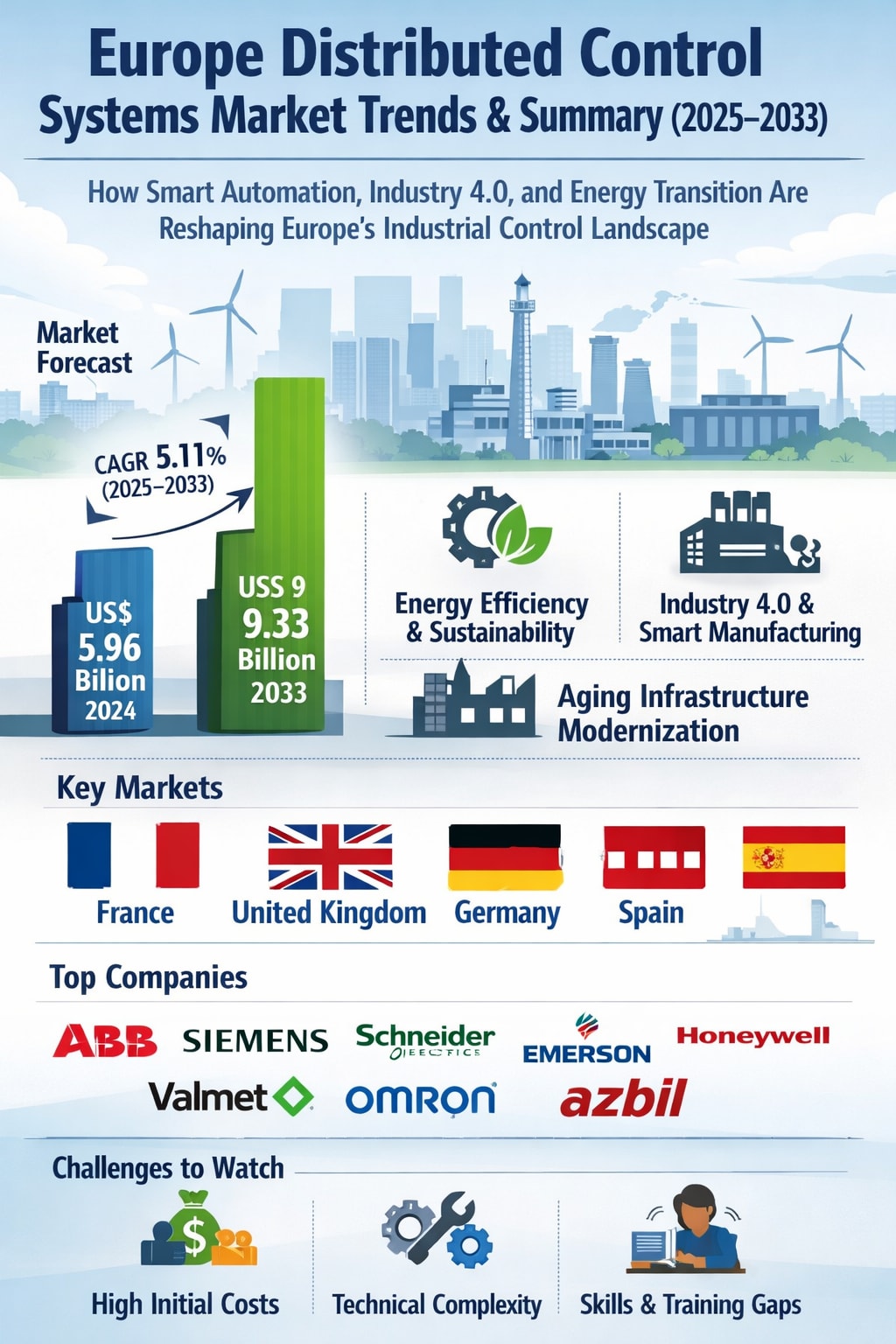

According to Renub Research, the Europe Distributed Control Systems Market is expected to grow from US$ 5.96 billion in 2024 to US$ 9.33 billion by 2033, registering a CAGR of 5.11% from 2025 to 2033. This steady expansion reflects not only the modernization of Europe’s industrial base but also the rising importance of interoperability, data-driven operations, and resilient automation systems.

Modern DCS architectures are no longer isolated control tools. They now integrate smoothly with SCADA systems, PLCs, enterprise software, and IoT platforms, creating a cooperative and highly data-driven control environment. This enhanced interoperability is attracting companies that manage complex, multi-layered processes and need unified control, visibility, and decision-making capabilities across their operations.

As Europe pushes forward with decarbonization goals, Industry 4.0 strategies, and infrastructure upgrades, DCS solutions are becoming central to the region’s industrial future.

Europe Distributed Control Systems Industry Overview

Distributed Control Systems play a critical role in Europe’s industrial automation ecosystem. By distributing control functions across a network rather than relying on a single centralized controller, DCS platforms significantly improve system reliability, operational efficiency, and process stability. This approach is especially valuable in large-scale and complex environments such as power plants, chemical facilities, refineries, pharmaceutical manufacturing units, and food processing plants.

Europe’s strong industrial foundation, combined with strict safety standards and regulatory requirements, has historically driven the adoption of advanced control technologies. Today, that momentum is accelerating as governments and enterprises invest heavily in digital transformation, real-time data monitoring, advanced analytics, and IoT-enabled operations.

Another powerful influence is Europe’s energy and environmental transition. The rapid expansion of renewable energy—particularly wind, solar, and hydropower—is pushing energy producers to adopt scalable and flexible automation systems. DCS platforms help manage the complexity of intermittent power generation, grid stability, and integrated energy networks.

At the same time, the rise of Industry 4.0 and smart manufacturing is increasing demand for integrated control systems that offer cybersecurity, remote monitoring, predictive maintenance, and advanced optimization tools. Leading players such as Siemens, ABB, Schneider Electric, and Honeywell continue to innovate, delivering more open, secure, and data-centric DCS platforms tailored to Europe’s evolving industrial needs.

As the region moves toward decarbonization, digitalization, and resilience, the DCS market is set to remain a cornerstone of Europe’s industrial modernization.

Policy Support and Digital Push: The UK Example

Government initiatives are playing a crucial role in accelerating automation adoption across Europe. A notable example is the United Kingdom’s commitment to transforming its manufacturing sector through smart technologies. In September 2020, the UK government announced USD 200.64 million in funding for the second phase of the “Manufacturing Made Smarter” program, aimed at boosting innovation, connectivity, and digital adoption in manufacturing.

Such initiatives directly benefit the DCS market by encouraging industries to modernize operations, integrate digital control systems, and improve efficiency through automation. Similar policy-driven digitalization efforts across Europe are reinforcing long-term demand for advanced control systems.

Growth Drivers for the Europe Distributed Control Systems Market

1. Rising Demand for Energy Efficiency and Sustainability

One of the strongest forces behind DCS adoption in Europe is the region’s commitment to sustainability and energy efficiency. The European Union’s ambitious climate targets and strict environmental regulations are pushing industries to reduce emissions, cut waste, and optimize energy consumption.

DCS platforms enable precise process control, real-time performance monitoring, and advanced analytics, helping companies improve efficiency and minimize resource losses. In sectors such as power generation, chemicals, and oil & gas, these capabilities translate directly into lower energy use, improved compliance, and reduced environmental impact.

By supporting automated optimization and continuous improvement, DCS systems have become a key enabler of sustainable industrial operations across Europe.

2. Industry 4.0 and Smart Manufacturing Initiatives

Europe’s strong push toward Industry 4.0 is another major driver of the DCS market. Manufacturers are increasingly adopting smart automation, connected machines, and data-driven decision-making to stay competitive in global markets.

Modern DCS solutions offer real-time data integration, production line control, advanced diagnostics, and predictive maintenance. These features help reduce downtime, improve product quality, and increase overall equipment effectiveness.

As factories become more connected and intelligent, DCS platforms serve as the central nervous system that coordinates machines, processes, and operators—making them indispensable to Europe’s smart manufacturing journey.

3. Modernization of Aging Infrastructure

A significant portion of Europe’s industrial infrastructure is aging and in need of modernization. Many facilities still rely on legacy control systems that are less reliable, harder to maintain, and limited in functionality.

Upgrading to modern DCS platforms offers a scalable and flexible way to improve performance without completely overhauling existing assets. New systems bring features such as remote monitoring, real-time analytics, and predictive maintenance, which help reduce downtime and prevent costly failures.

This modernization trend is particularly strong in oil & gas, chemicals, and power generation, where operational reliability and safety are mission-critical.

Challenges in the Europe Distributed Control Systems Market

1. High Initial Investment Costs

Despite their long-term benefits, DCS solutions require significant upfront investment. Costs include hardware, software, system integration, infrastructure upgrades, and workforce training. For small and medium-sized enterprises (SMEs), these expenses can be a major barrier.

Even though DCS can deliver strong returns through efficiency gains and reduced downtime, the high initial capital requirement often delays or limits adoption, especially among budget-constrained organizations.

2. Technological Complexity and Training Requirements

DCS platforms are technically sophisticated, requiring skilled personnel for operation, maintenance, and troubleshooting. Companies must invest in specialized training programs, which increases costs and can slow down implementation.

Additionally, as DCS technology evolves rapidly, organizations need to continuously update systems and skills, creating ongoing challenges in workforce development and change management.

Country-Level Market Insights

France

France’s DCS market is driven by manufacturing, chemicals, and energy sectors. The country’s strong focus on modernization and sustainability is accelerating the replacement of legacy systems with advanced DCS platforms. Industry 4.0 initiatives and strict environmental regulations are further boosting demand for intelligent, efficient, and compliant control solutions.

United Kingdom

The UK DCS market plays a vital role in industries such as food processing, energy, chemicals, and pharmaceuticals. Government-backed programs like Manufacturing Made Smarter are encouraging digital adoption, while industries seek automation solutions to improve productivity, quality, and regulatory compliance.

Germany

Germany stands at the forefront of industrial automation and Industry 4.0. DCS systems are widely used across manufacturing, energy, chemicals, and pharmaceuticals to enable real-time monitoring and process optimization. Strong emphasis on energy efficiency, sustainability, and digital transformation continues to drive market growth, although cybersecurity and skills shortages remain key challenges.

Spain

Spain’s DCS market is benefiting from government support for digital transformation and ambitious renewable energy targets. The expansion of wind and solar capacity is increasing the need for advanced control systems to manage complex energy networks, positioning DCS as a critical technology for the country’s industrial and energy future.

Europe Distributed Control Systems Market Segmentation

By Component:

Hardware

Software

Services

By End User:

Oil & Gas

Power Generation

Chemicals

Food & Beverages

Pharmaceuticals

Metals & Mining

Paper & Pulp

Others

By Country:

France

Germany

Italy

Spain

United Kingdom

Belgium

Netherlands

Russia

Poland

Greece

Norway

Romania

Portugal

Rest of Europe

Competitive Landscape and Company Analysis

The European DCS market is highly competitive and innovation-driven. Key players are focusing on open architectures, cybersecurity, digital integration, and lifecycle services to strengthen their market positions.

Major Companies Covered:

ABB

Siemens AG

Azbil Corporation

Schneider Electric SE

Valmet Oyj

Omron Corporation

Emerson Electric Co

Honeywell International Inc.

These companies are analyzed across:

Company Overview

Key Executives

Recent Developments

Revenue Performance

Their strategies increasingly revolve around digital platforms, software-centric control systems, cloud integration, and advanced analytics, reflecting the broader shift toward smart and connected industrial operations.

Market Outlook: What Lies Ahead?

Looking forward, the Europe Distributed Control Systems market is set to play a central role in the region’s industrial transformation. The combination of energy transition, Industry 4.0 adoption, infrastructure modernization, and sustainability goals will continue to fuel demand for advanced control solutions.

While challenges such as high costs and skills gaps remain, the long-term benefits of improved efficiency, resilience, and digital integration make DCS a strategic investment for European industries.

With the market projected to reach US$ 9.33 billion by 2033, DCS will remain a critical enabler of Europe’s journey toward smarter, cleaner, and more competitive industrial operations.

Final Thoughts

The Europe Distributed Control Systems market is no longer just about automation—it’s about intelligent orchestration of complex industrial ecosystems. As industries strive for sustainability, efficiency, and digital excellence, DCS platforms are becoming the silent architects behind Europe’s industrial future. For companies willing to invest in modernization and skills, the rewards will be measured not only in productivity gains but also in long-term resilience and competitiveness.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

North America Salmon Fish Market Trends & Summary (2025–2033)

North America Salmon Fish Market at a Glance The North America Salmon Fish Market is entering a strong growth phase, reflecting changing consumer lifestyles, rising health awareness, and the rapid evolution of seafood supply chains. According to Renub Research, the market is expected to expand from US$ 6.22 billion in 2024 to US$ 12.33 billion by 2033, growing at a CAGR of 7.90% from 2025 to 2033.

By shibansh kumarabout 5 hours ago in Trader

Philippines Adult Diaper Market 2026: Set for Steady Growth Amid Aging Population and Healthcare Expansion

Philippines Adult Diaper Market Overview The Philippines adult diaper market is quietly emerging as a stable and steadily expanding sector within the broader personal care and healthcare landscape. According to IMARC Group’s latest research, the market generated USD 97.53 million in revenue in 2025 and is forecast to reach USD 145.09 million by 2034, growing at a compound annual growth rate (CAGR) of 4.51% between 2026 and 2034.

By Manisha Dixit4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.