UK Mortgage Rates Today 2026 – Latest Fixed & Variable Interest Trends

Stay updated on UK mortgage rates in 2026, including fixed and variable interest trends

Introduction

UK mortgage rates are one of the first things people check when they plan to buy a home or remortgage in 2026.

Many borrowers want clear answers about what is happening now and what may come next, without confusing terms or complex explanations.

This guide explains the current situation in simple English. It is written for everyday readers who want practical help and real understanding before making a big financial choice.

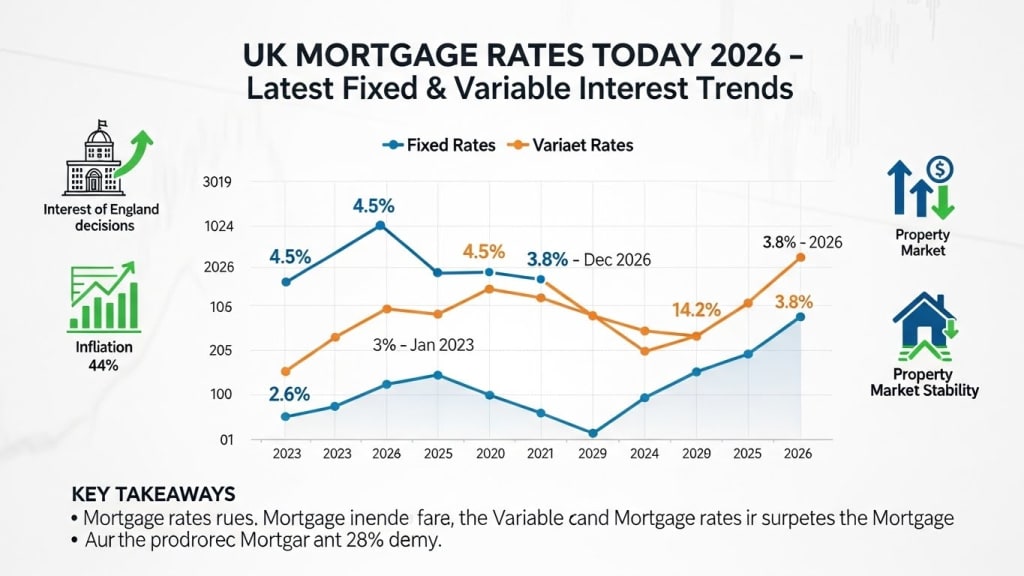

The Current Market Picture in 2026

Mortgage lending in 2026 feels more balanced than in past years. Lenders are offering more options, and buyers have time to compare deals calmly.

Small changes in interest levels still matter. Even a tiny shift can change monthly payments, which is why staying informed is so important.

UK Mortgage Rates Explained for Homebuyers

UK mortgage rates reflect how much interest you pay to borrow money for a home. These rates depend on lender costs, market confidence, and the wider economy.

For most people, the rate directly affects affordability. Lower rates mean smaller monthly payments, while higher rates can limit borrowing power.

Fixed Rate Options and What They Mean

Fixed mortgages remain popular in 2026. They give peace of mind because payments stay the same for a set time.

Common fixed terms include:

Two-year fixes for flexibility

Five-year fixes for stability

Longer fixes for long-term planners

These options suit people who like predictable budgets.

Variable and Tracker Choices in Focus

Variable deals can move up or down over time. They often follow the base rate, which means payments may change.

Some borrowers like this risk because:

Rates may fall later

Early repayment fees are often lower

Deals can feel more flexible

Still, payment changes can be stressful for some households.

How the Base Rate Shapes Lending Decisions

The Bank of England base rate plays a big role in lending costs. When it changes, lenders often adjust their offers.

In 2026, the base rate has shown steadier movement. This has helped calm fears and allowed lenders to plan more clearly.

First-Time Buyers and Entry-Level Deals

First-time buyers face unique challenges. Deposits are still a major hurdle, even when rates look fair.

Helpful options include:

Low-deposit mortgages

Government-backed support schemes

Family-assisted deposits

These choices make entering the market more realistic for new buyers.

Buy-to-Let Borrowing in 2026

Landlords are watching costs closely this year. Rental income must cover mortgage payments comfortably.

Many investors prefer:

Shorter fixed terms

Flexible overpayment options

Clear exit fees

Careful planning is essential to protect long-term returns.

Remortgaging: When and Why It Helps

Remortgaging can reduce costs or improve terms. Many homeowners review deals before their current fix ends.

Reasons people remortgage include:

Lower monthly payments

Access to better interest terms

Releasing equity for home upgrades

Timing matters, so early planning pays off.

Regional Differences Across the UK

Mortgage costs can feel different depending on where you live. Property prices and local demand both affect lending choices.

In high-demand areas, borrowers often need larger deposits. In quieter regions, lenders may offer more flexible terms.

Affordability Checks and Lending Rules

Lenders now focus strongly on affordability. They look at income, spending habits, and future risks.

This protects borrowers from over-committing. It also helps ensure mortgages remain manageable over time.

Digital Tools Changing the Mortgage Journey

Online tools make comparing deals easier than ever. Many people now research from home before speaking to an adviser.

Popular tools include:

Mortgage calculators

Comparison websites

Online lender portals

These tools save time and build confidence.

Long-Term Outlook for Borrowers

The outlook for homeowners in 2026 feels steadier than before. Sudden shocks are less common, which helps planning.

Experts expect gradual change rather than sharp swings. This supports smarter, calmer decision-making.

Common Mistakes to Avoid

Some mistakes still catch borrowers out. Being aware can save money and stress.

Avoid:

Ignoring small print

Focusing only on the headline rate

Forgetting fees and charges

A full view always beats a quick choice.

Final Thoughts

UK mortgage rates remain a key factor for buyers, owners, and investors in 2026. Understanding how fixed and variable options work helps you choose with confidence.

By comparing deals, planning ahead, and staying informed, you can make better decisions and protect your finances for the future.

Comments

There are no comments for this story

Be the first to respond and start the conversation.