United States Automotive Service Market Size and Forecast 2025–2033

How Aging Vehicles, EVs, and Smart Diagnostics Are Reshaping America’s Auto Service Industry

Introduction

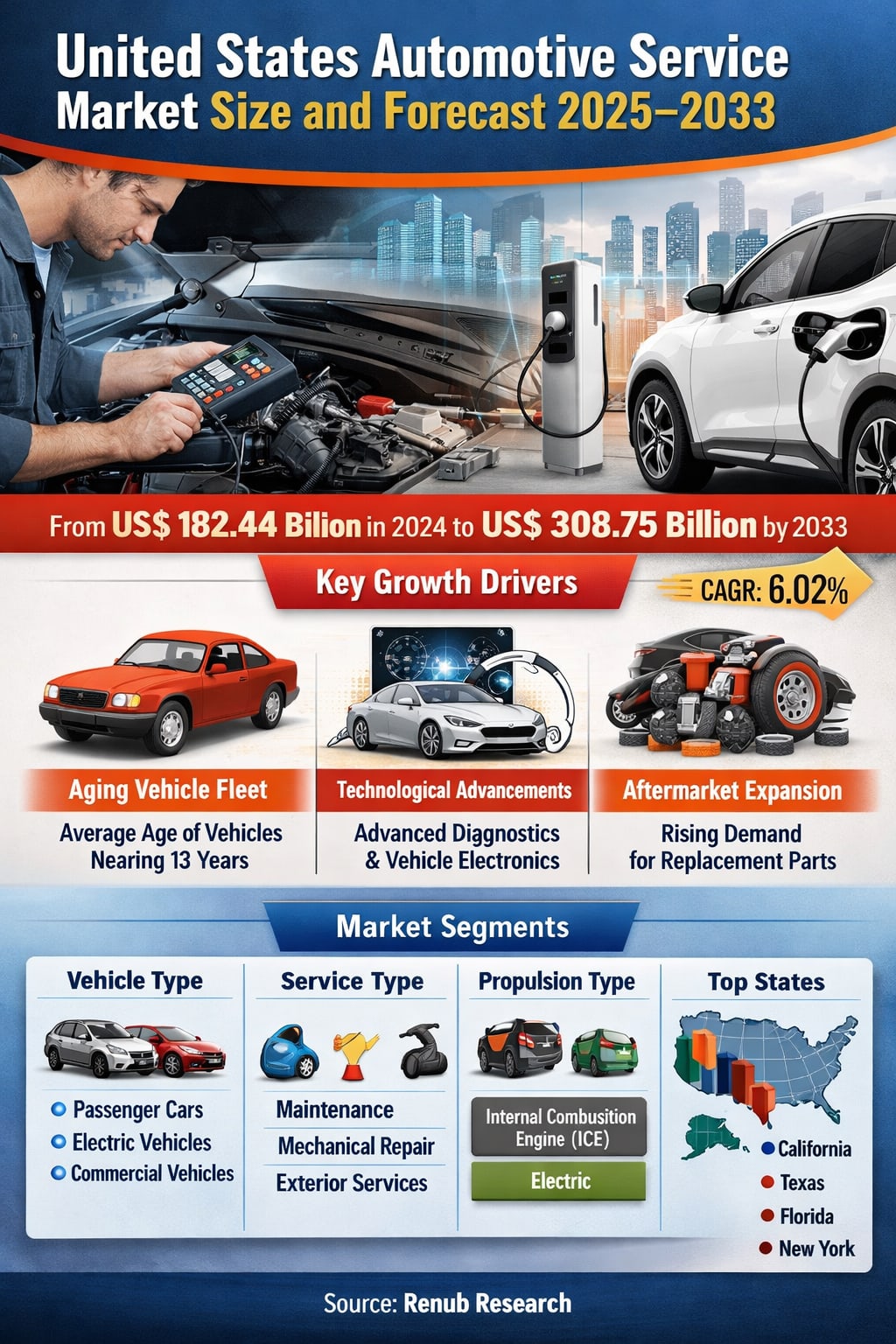

The United States automotive service market is entering a transformative decade. As vehicles become more technologically complex and the national car fleet continues to age, the demand for professional maintenance, diagnostics, and repair services is rising steadily. According to Renub Research’s latest analysis, the United States Automotive Service Market is expected to reach US$ 308.75 billion by 2033, up from US$ 182.44 billion in 2024, growing at a CAGR of 6.02% from 2025 to 2033.

This growth reflects more than just routine oil changes and tire rotations. Today’s automotive service industry sits at the intersection of digital diagnostics, electric mobility, software-driven vehicles, and changing consumer expectations. From independent garages and dealership service centers to quick-service chains and mobile repair platforms, the ecosystem is expanding and modernizing to meet new challenges.

The sector plays a critical role in keeping America’s vast vehicle population safe, efficient, and roadworthy. Whether it is maintaining internal combustion engine (ICE) vehicles, servicing electric vehicles (EVs), or repairing increasingly sophisticated electronic systems, automotive service providers are becoming as technology-driven as the vehicles they maintain. In many ways, the future of mobility in the United States depends not only on how cars are built, but also on how well they are serviced throughout their lifespan.

United States Automotive Service Industry Overview

Automotive service encompasses all repair, maintenance, and inspection activities performed to ensure the safety, performance, and longevity of vehicles. This includes routine services such as oil changes, brake inspections, tire replacements, and fluid checks, as well as complex repairs involving engines, transmissions, electrical systems, and software-controlled components.

As modern vehicles integrate advanced electronics, sensors, and software, the nature of automotive servicing has changed dramatically. Today’s technicians must be trained not only in mechanical systems but also in diagnostics, data interpretation, and electronic calibration. The industry now relies heavily on advanced diagnostic tools, computerized testing equipment, and manufacturer-specific software platforms.

Both personal and commercial vehicles depend on these services to remain compliant with safety standards, maintain fuel efficiency, and reduce the risk of breakdowns. In economic terms, the automotive service industry also supports millions of jobs across the United States, from technicians and engineers to parts suppliers and logistics providers.

Several structural factors are driving the steady expansion of the market. The average age of vehicles on U.S. roads is now close to 13 years, which naturally increases the frequency and complexity of maintenance needs. At the same time, the rise of electric vehicles is introducing new service categories, such as battery diagnostics, high-voltage system maintenance, and specialized software updates. Together, these trends are reshaping what it means to “service” a vehicle in the modern era.

Market Size and Growth Outlook

Renub Research projects a strong and sustained growth trajectory for the U.S. automotive service market. The industry is expected to expand from US$ 182.44 billion in 2024 to US$ 308.75 billion by 2033, registering a CAGR of 6.02% during the period 2025 to 2033.

This growth is underpinned by multiple long-term trends. First, vehicle ownership in the United States remains high, ensuring a large and stable customer base for maintenance and repair services. Second, consumers are keeping their vehicles longer, partly due to higher new car prices and economic uncertainty, which increases spending on repairs and upkeep. Third, technological advancements are making vehicles more complex, raising both the frequency of service visits and the value of each service transaction.

In addition, the shift toward electric and hybrid vehicles is not reducing the importance of service providers—rather, it is changing the nature of the services they offer. While EVs may require less frequent mechanical maintenance, they demand specialized expertise in batteries, power electronics, and software systems. This creates new revenue streams for service centers that are willing to invest in training and equipment.

Taken together, these factors suggest that the U.S. automotive service market is not only growing in size, but also evolving in scope and sophistication.

Key Growth Drivers

Increasing Average Age of Vehicles

One of the most powerful drivers of market growth is the rising average age of vehicles in the United States. With many cars and trucks remaining in service for over a decade, the need for regular maintenance and periodic major repairs is increasing. Older vehicles typically require more frequent attention, including suspension repairs, brake system overhauls, engine tune-ups, and replacement of worn components.

As consumers choose to extend the life of their existing vehicles rather than purchase new ones, service providers benefit from a steady stream of demand. Older vehicles also tend to experience more complex wear-related issues, which often require advanced diagnostics and skilled labor. This trend supports not only higher service volumes but also higher-value repair jobs, strengthening overall market revenues.

Rapid Technological Advancements in Vehicle Electronics and Diagnostics

Modern vehicles are increasingly defined by software and electronics. Advanced driver-assistance systems (ADAS), infotainment platforms, connected car features, and sophisticated engine management systems have become standard across many segments. While these technologies improve safety and performance, they also make servicing more complex.

Routine maintenance today often involves computerized diagnostics, firmware updates, sensor calibrations, and electronic troubleshooting. This complexity increases the reliance on professional service centers equipped with the right tools and expertise. It also encourages service providers to invest in continuous training and advanced equipment, raising the overall technological standard of the industry. As a result, technological progress is not only reshaping vehicles but also expanding the scope and value of automotive services.

Expansion of Aftermarket Automotive Parts and Services

The growth of the aftermarket sector is another important driver. As vehicles age, the demand for replacement parts and cost-effective repair solutions increases. Many consumers prefer aftermarket parts because they are often more affordable and widely available than original equipment manufacturer (OEM) components.

Supportive regulatory environments, including Right to Repair initiatives, have improved access to repair information and parts, fostering competition and innovation within the service industry. At the same time, advancements in aftermarket components—such as improved durability and better compatibility—are making them an increasingly attractive option for both consumers and service providers. This combination of affordability, accessibility, and innovation is fueling steady expansion in aftermarket services across the country.

Challenges Facing the Market

Intense Competition

The U.S. automotive service industry is highly competitive. Dealership service departments, independent repair shops, national quick-service chains, and emerging mobile service platforms all compete for the same customer base. This intense competition puts pressure on pricing and profit margins, especially as consumers become more price-sensitive and convenience-driven.

To stay competitive, service providers must invest in technology, skilled technicians, and customer experience improvements. While these investments are necessary, they also increase operating costs and complexity. The challenge for many businesses is to balance affordability with quality while maintaining sustainable profitability in a crowded marketplace.

Supply Chain Disruptions

Supply chain instability has become a significant challenge for the automotive service sector. Delays in the availability of parts and components can extend repair times, frustrate customers, and lead to lost revenue. These disruptions can stem from global manufacturing slowdowns, transportation bottlenecks, or geopolitical uncertainties.

Service providers are often forced to hold higher inventory levels, seek alternative suppliers, or pay premiums for expedited shipping. All of these measures increase costs and complicate operations. In an industry where customer trust and turnaround time are critical, supply chain reliability has become a key operational concern.

Recent Developments in the U.S. Automotive Service Industry

The market has witnessed notable strategic moves in recent years, reflecting ongoing consolidation and expansion efforts:

December 2022: AutoNation Inc., one of the largest automotive retailers in the United States, acquired RepairSmith, a full-service mobile vehicle repair and maintenance company based in Los Angeles with operations across the southern and western U.S. This move highlights the growing importance of mobile and on-demand service models.

May 2022: Monro, Inc. and American Tire Distributors announced a final agreement under which American Tire Distributors would acquire Monro’s wholesale tire distribution assets, to be operated under the “Tires Now” name. This transaction underscores the strategic value of distribution networks in the service ecosystem.

March 2022: Monro, Inc. expanded its footprint by acquiring Mountain View Tire & Service Inc., adding 116 locations and approximately US$ 45 million in expected annual sales. This acquisition reflects the ongoing consolidation trend aimed at achieving scale and regional strength.

Market Segmentation

By Vehicle Type

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Passenger cars continue to dominate service volumes, but electric vehicles represent the fastest-evolving segment, with unique service requirements related to batteries and software systems.

By Service Type

Mechanical Services

Maintenance Services

Exterior/Structural Services

While routine maintenance remains a core revenue source, mechanical and structural repairs are becoming more technology-intensive and higher in value.

By Propulsion Type

Internal Combustion Engine (ICE)

Electric

ICE vehicles still account for the majority of service demand, but the electric segment is growing steadily as EV adoption increases across the United States.

By States

California

Texas

New York

Florida

Illinois

Pennsylvania

Ohio

Georgia

Washington

New Jersey

Rest of United States

Large, populous states with high vehicle ownership naturally generate the greatest service demand, but growth opportunities exist nationwide as mobility patterns evolve.

Competitive Landscape

The U.S. automotive service market features a mix of large national chains, regional players, and independent operators. Key players include:

Firestone Complete Auto Care

Jiffy Lube International, Inc.

Meineke Car Care Centers, LLC

Midas International, LLC

Monro Inc.

Safelite Group

Walmart Inc.

Pep Boys

These companies are typically analyzed across multiple dimensions, including company overview, key leadership, recent developments and strategies, SWOT analysis, and sales performance. Scale, brand recognition, and service network reach remain critical competitive advantages, while digital booking platforms and customer experience innovations are becoming increasingly important differentiators.

The Road Ahead

Looking forward, the U.S. automotive service industry is set to become even more technology-driven. The integration of connected vehicle data, predictive maintenance systems, and advanced diagnostics will continue to reshape service models. Electric and autonomous vehicles will introduce new skill requirements and business opportunities, while traditional ICE vehicles will still demand extensive maintenance as long as they remain on the road.

Service providers that invest early in training, digital tools, and customer-centric models are likely to gain a competitive edge. At the same time, consolidation is expected to continue, as larger players seek scale, efficiency, and broader geographic coverage.

Despite challenges related to competition and supply chains, the long-term fundamentals of the market remain strong. Vehicle ownership is deeply embedded in American life, and as long as vehicles exist, the need for reliable, professional service will remain essential.

Final Thoughts

The United States Automotive Service Market, projected to grow from US$ 182.44 billion in 2024 to US$ 308.75 billion by 2033 at a CAGR of 6.02%, stands as a cornerstone of the nation’s mobility ecosystem. Driven by an aging vehicle fleet, rapid technological advancements, expanding aftermarket services, and the rise of electric vehicles, the industry is evolving into a more sophisticated, technology-oriented sector.

While challenges such as intense competition and supply chain disruptions persist, the overall outlook remains positive. The automotive service industry is not just keeping pace with changes in vehicle technology—it is becoming a critical enabler of the future of transportation in the United States. For businesses, investors, and consumers alike, this market represents both stability and transformation in equal measure.

About the Creator

Global Vitamin K2 Market Size and Forecast (2025–2033)

Introduction: A Quiet Vitamin with a Powerful Market Story The global health and wellness industry is undergoing a profound transformation. Consumers today are no longer satisfied with reactive healthcare alone; instead, they are increasingly investing in preventive solutions that promise long-term vitality, better quality of life, and reduced risk of chronic disease. Within this shifting landscape, vitamin K2 has emerged as one of the most promising yet previously underappreciated nutrients.

By shibansh kumar4 days ago in Trader

Huawei Stock Outlook: Investment Perspective and Growth Potential

Introduction Huawei Technologies Co., Ltd. is one of the world’s largest technology companies, dominating telecommunications, smartphones, cloud computing, and 5G infrastructure. Despite being a privately held company, Huawei’s technological innovation, global expansion, and strategic positioning make it a key focus for investors tracking the global tech and telecom sectors.

By Hammad Nawaza day ago in Trader

At My Wits’ End

Life is about taking out the trash and calling it trash because you have every reason to. It wasn't meant to be linear, they say. But the times you tried to make it straight led to problems, and you didn’t have the tools to put any of it to use. You don't put your right shoes on the right feet; you put the left shoes on the left feet. The grey hardened slab will trip you up anyway.

By Caitlin Charltona day ago in Humans

Comments

There are no comments for this story

Be the first to respond and start the conversation.