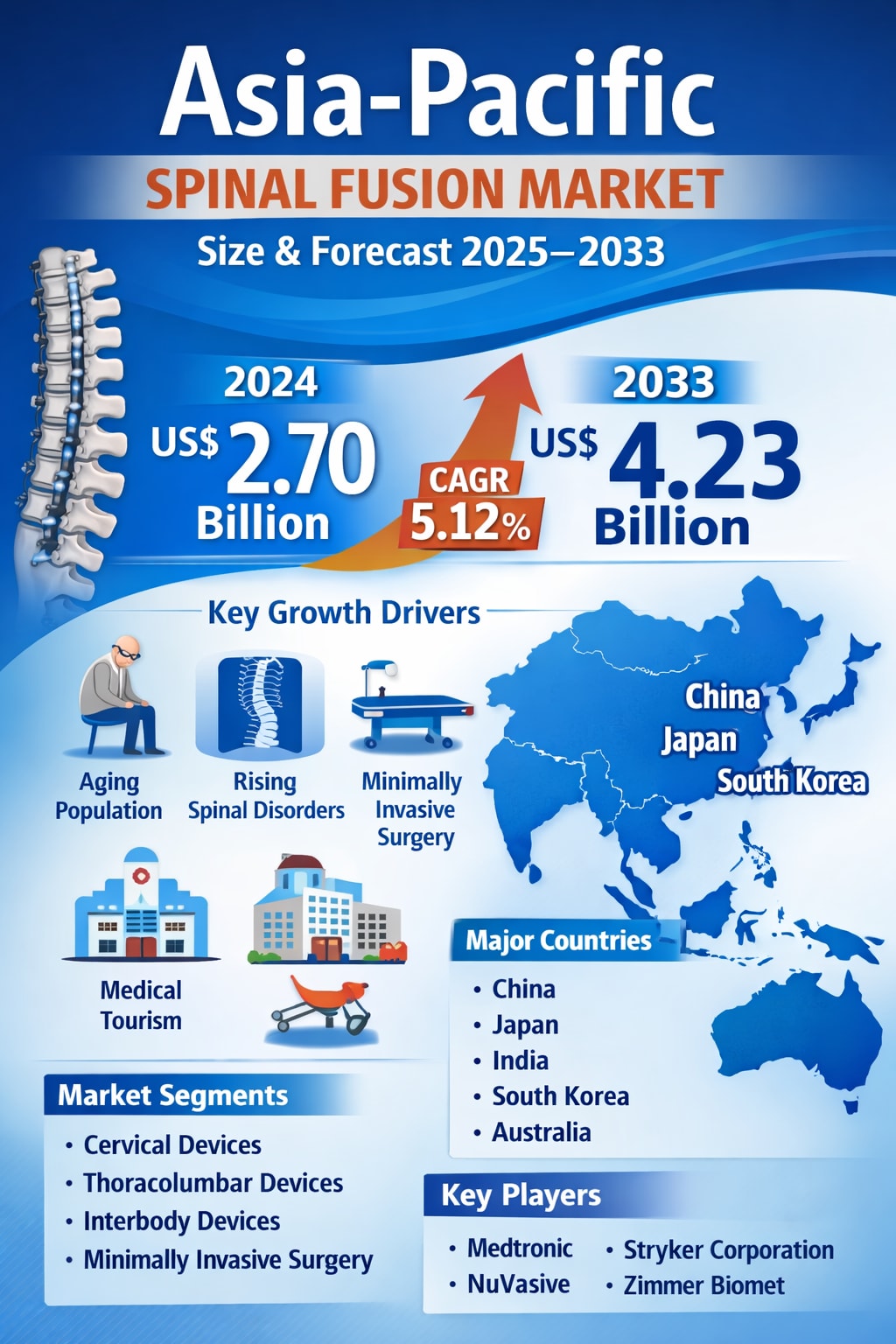

Asia-Pacific Spinal Fusion Market Size and Forecast 2025–2033

How Aging Populations, Medical Tourism, and Minimally Invasive Surgery Are Reshaping Spine Care Across the Region

Introduction: A Region at the Center of Spine Surgery Growth

The Asia-Pacific spinal fusion market is entering a decisive decade of expansion, driven by demographic change, technological progress, and rising demand for advanced orthopedic care. The market is expected to reach US$ 4.23 billion by 2033, up from US$ 2.70 billion in 2024, growing at a compound annual growth rate (CAGR) of 5.12% from 2025 to 2033.

This growth is not happening in isolation. Across countries such as China, Japan, India, South Korea, Australia, and Southeast Asia, healthcare systems are undergoing rapid modernization. Aging populations, increasing prevalence of spinal disorders, greater awareness of spine health, and rising healthcare spending are converging to push spinal fusion procedures into the mainstream of orthopedic and neurosurgical practice.

Spinal fusion, a surgical technique used to join two or more vertebrae to stabilize the spine and relieve pain, has become a critical treatment option for conditions such as degenerative disc disease, spinal stenosis, scoliosis, and traumatic spinal injuries. As lifestyles become more sedentary, life expectancy increases, and diagnostic capabilities improve, the pool of patients eligible for these procedures continues to expand.

At the same time, the region is benefiting from rapid technological innovation. Robotic-assisted surgery, navigation systems, bioresorbable materials, and 3D-printed implants are improving surgical precision and reducing recovery times. Combined with the rise of minimally invasive spine surgery (MISS), these advances are making spinal fusion safer, more efficient, and more acceptable to patients who previously might have avoided surgery.

Medical tourism is another powerful catalyst. Countries such as India and Thailand are attracting international patients with high-quality care at comparatively affordable costs, further boosting procedure volumes and encouraging hospitals to invest in advanced spine surgery capabilities. Despite challenges such as high device costs and regulatory hurdles in some markets, the Asia-Pacific region is firmly positioning itself as one of the most dynamic growth engines in the global spinal fusion landscape.

Market Overview: Why Demand Is Rising Across Asia-Pacific

The Asia-Pacific spinal fusion market is expanding on the back of several long-term structural trends. One of the most important is the rapid aging of the population. Japan already has one of the oldest populations in the world, and countries like China and South Korea are following closely behind. As people age, degenerative spinal conditions become more common, significantly increasing the need for surgical interventions such as spinal fusion.

Urbanization and changing lifestyles are also playing a role. Long hours of desk work, reduced physical activity, and higher rates of obesity are contributing to back pain, disc degeneration, and spinal instability. In parallel, better access to diagnostic imaging such as MRI and CT scans is leading to earlier and more accurate detection of spinal disorders, which in turn increases the number of patients considered for surgical treatment.

Rising healthcare expenditure across emerging economies is making advanced procedures more accessible. Governments and private investors are pouring funds into hospital infrastructure, specialty clinics, and medical training programs. This is not only improving access in major cities but also gradually extending advanced spine care into semi-urban areas.

Technological progress is reshaping clinical practice. Innovations such as robotic-assisted surgery, advanced navigation systems, and improved implant materials are helping surgeons achieve better outcomes with fewer complications. These developments are also shortening hospital stays and recovery times, making spinal fusion a more attractive option for both patients and healthcare providers.

In early 2024, Stryker Corporation expanded its footprint in India by establishing additional spine surgeon training facilities in Pune and Chandigarh, focusing on robotics integration and navigation-assisted spinal fusion techniques. Around the same time, Johnson & Johnson Medical India introduced the SYMPHONY™ OCT System, designed to enhance visibility and precision during complex spine surgeries, accompanied by a comprehensive surgeon training program in major hospitals. These kinds of initiatives highlight how global players are investing in skills development and technology adoption across the region.

Key Growth Drivers Shaping the Market

Rising Prevalence of Spinal Disorders

One of the most powerful forces behind market growth is the increasing incidence of spinal disorders. Conditions such as degenerative disc disease, herniated discs, scoliosis, and spinal trauma are becoming more common due to aging, sedentary lifestyles, and physically demanding work environments. These conditions often lead to chronic pain, reduced mobility, and a diminished quality of life, creating a strong demand for effective long-term treatment options.

Spinal fusion is widely regarded as a reliable solution for stabilizing the spine and relieving pain in severe cases. As awareness of these conditions and their treatment options improves, more patients are opting for surgical intervention. This trend is visible across both developed and developing Asia-Pacific markets, contributing to a steady rise in procedure volumes.

Surge in Minimally Invasive Surgeries

The shift toward minimally invasive spine surgery is another major growth catalyst. Compared to traditional open procedures, minimally invasive techniques involve smaller incisions, less muscle damage, reduced blood loss, and shorter hospital stays. Patients typically experience less postoperative pain, faster recovery, and better overall satisfaction.

Advancements in surgical instruments, imaging technologies, and navigation systems have made these procedures more precise and widely available. As a result, both surgeons and patients are increasingly favoring minimally invasive approaches, which is driving demand for specialized devices and implants designed for these techniques.

Improved Healthcare Infrastructure

Healthcare infrastructure across Asia-Pacific has improved significantly over the past decade. Governments are investing heavily in new hospitals, upgrading existing facilities, and expanding access to specialized care. The growth of private healthcare providers and specialty clinics is also increasing the availability of advanced orthopedic and spinal procedures.

In parallel, the expansion of medical education and training programs is producing more skilled surgeons, which directly supports the growth of complex procedures such as spinal fusion. As infrastructure and human resources continue to improve, a larger portion of the population is gaining access to high-quality spine care.

Challenges That Continue to Restrain the Market

High Procedure and Device Costs

Despite strong demand, high costs remain a significant barrier. Spinal fusion procedures often require expensive implants, advanced surgical tools, and specialized equipment. In many Asia-Pacific countries, a large share of healthcare expenses is still paid out of pocket, which limits access for a substantial portion of the population.

Even when surgery is medically necessary, financial constraints can delay or prevent treatment. This issue is particularly pronounced in developing economies, where insurance coverage may be limited and public healthcare budgets are under pressure. Cost containment and broader reimbursement coverage will be critical for unlocking the market’s full potential.

Post-Surgical Complications and Risks

Although surgical techniques have improved, spinal fusion is still associated with risks such as infection, nerve damage, blood clots, and failed fusion, where the bones do not properly join. Some patients may also experience persistent pain or limited mobility even after surgery.

These risks can make patients hesitant to choose surgical intervention, especially when outcomes are uncertain. Improving surgical techniques, enhancing patient selection, and strengthening postoperative care and rehabilitation programs will be essential for building confidence in spinal fusion procedures.

Country-Level Insights: Growth Stories Across the Region

China

China’s spinal fusion market is growing rapidly, supported by an aging population, rising incidence of spinal disorders, and continuous improvements in healthcare infrastructure. Minimally invasive procedures are gaining popularity, and more hospitals are adopting advanced surgical technologies. However, high costs and a shortage of highly skilled specialists remain challenges. Government initiatives to modernize healthcare and promote medical technology adoption are expected to sustain long-term growth.

Japan

Japan’s market is strongly influenced by its aging demographics, with over 29% of the population aged 65 and older. Degenerative spinal conditions are increasingly common, driving demand for spinal fusion surgeries. Technological innovations, including robotic-assisted and minimally invasive techniques, are improving outcomes and reducing recovery times. While high costs and workforce constraints persist, strong government support for healthcare innovation continues to underpin market expansion.

India

India’s spinal fusion market is expanding robustly due to a growing elderly population, rising awareness of spine health, and rapid adoption of advanced surgical technologies. The country is also a major hub for medical tourism, attracting patients seeking high-quality care at competitive prices. Initiatives to improve healthcare infrastructure and promote medical technology innovation are supporting growth, although affordability and access remain key challenges.

South Korea

South Korea is emerging as a regional center for advanced spine surgery, supported by a well-developed healthcare system and strong medical tourism inflows. Minimally invasive techniques are increasingly popular, offering faster recovery and fewer complications. High device costs and the need for specialized surgical skills remain constraints, but ongoing investments in technology and training are strengthening the market’s long-term outlook.

Market Segmentation: How the Industry Is Structured

By Product Type (4 viewpoints):

Cervical Devices

Thoracolumbar Devices

Interbody Devices

Biologics

By Surgery Type (2 viewpoints):

Minimally Invasive Spine Surgery

Open Spine Surgery

By End User (3 viewpoints):

Hospitals

Specialty Clinics

Others

By Country (10 viewpoints):

China

Japan

India

South Korea

Thailand

Malaysia

Indonesia

Australia

New Zealand

Rest of Asia Pacific

Competitive Landscape: Key Companies in Focus

The Asia-Pacific spinal fusion market is highly competitive, with global and regional players investing heavily in product innovation, training, and market expansion. Major companies covered in the competitive analysis include:

Medtronic Plc.

Xtant Medical Holdings

Alphatec Holdings Inc.

Stryker Corporation

Zimmer Biomet Holdings

Orthofix Medical Inc.

NuVasive Inc.

Globus Medical Inc.

Bejo Zaden BV

Corteva Agriscience

These companies are evaluated across four key viewpoints: overview, key persons, recent developments, and revenue. Strategic partnerships, product launches, and investments in surgeon training are common strategies used to strengthen market presence and drive adoption of advanced spinal fusion technologies.

Outlook: What the Next Decade Holds

Looking ahead to 2033, the Asia-Pacific spinal fusion market is set to remain on a steady growth trajectory. The combination of demographic change, technological innovation, and expanding healthcare infrastructure creates a strong foundation for long-term expansion. Minimally invasive techniques, robotics, and advanced implant materials will continue to reshape clinical practice and improve patient outcomes.

At the same time, addressing challenges related to cost, access, and surgical risk will be crucial. Broader insurance coverage, cost-effective device solutions, and continued investment in training and infrastructure can help unlock the market’s full potential and ensure that more patients benefit from advanced spine care.

Final Thoughts

The Asia-Pacific spinal fusion market is moving into a new phase of maturity and innovation. With the market projected to grow from US$ 2.70 billion in 2024 to US$ 4.23 billion by 2033 at a CAGR of 5.12%, the region is clearly becoming one of the most important arenas for the future of spine surgery.

Driven by aging populations, rising disease burden, medical tourism, and rapid technological progress, spinal fusion is no longer a niche procedure reserved for a few advanced centers. It is increasingly becoming a core component of modern orthopedic and neurosurgical care across Asia-Pacific. For device manufacturers, healthcare providers, and policymakers alike, the coming decade offers both significant opportunities and important responsibilities in shaping a more accessible, effective, and patient-centered spine care ecosystem.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Asia-Pacific Yeast Market Trends & Summary

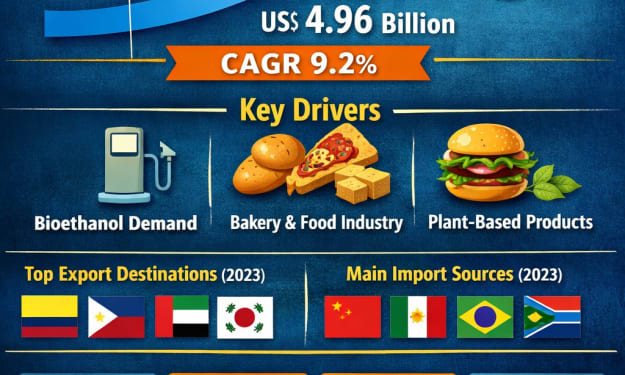

Introduction: A Fermentation Boom Across Asia-Pacific The Asia-Pacific yeast market is entering a decisive growth phase, driven by powerful shifts in food consumption, energy policies, and health-conscious consumer behavior. According to Renub Research, the Asia-Pacific Yeast Market is expected to reach US$ 4.96 billion by 2033, rising from US$ 2.25 billion in 2024, registering a strong CAGR of 9.2% from 2025 to 2033. This impressive trajectory reflects how yeast has moved beyond its traditional role in baking and brewing to become a critical input for bioethanol production, pharmaceuticals, animal feed, and functional nutrition.

By shibansh kumar3 days ago in Trader

Crypto Market Today: Bitcoin Slips to $67,233 as XRP Falls Below $2, Ethereum Nears $1,975

Introduction Cryptocurrency prices traded lower today as the market witnessed renewed selling pressure across major digital assets. Bitcoin slipped to $67,233, while XRP fell below the key $2 mark and Ethereum hovered near $1,975. The pullback comes amid cautious investor sentiment, profit booking after recent rallies, and uncertainty surrounding global macroeconomic signals.

By Hammad Nawaz4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.