Global STD Diagnostics Market Size & Forecast 2025–2033: Testing at the Frontline of Public Health

Rising awareness, rapid diagnostics, and molecular breakthroughs drive the global STD diagnostics market from US$ 16.82 billion in 2024 to US$ 30.84 billion by 2033

Introduction: Why STD Diagnostics Matter More Than Ever

According to Renub Research’s latest industry analysis, the Global STD Diagnostics Market is projected to grow from US$ 16.82 billion in 2024 to US$ 30.84 billion by 2033, expanding at a CAGR of 6.97% during 2025–2033. This impressive growth reflects not only rising infection rates worldwide but also a profound shift in how societies approach sexual health, prevention, and early diagnosis.

Sexually transmitted diseases (STDs) remain one of the most persistent public health challenges across both developed and developing nations. Infections such as chlamydia, gonorrhea, syphilis, HIV, HPV, and herpes affect millions each year, often silently. Many of these conditions can remain asymptomatic for long periods, quietly increasing the risk of severe complications such as infertility, chronic pain, organ damage, and in some cases, death.

STD diagnostics, therefore, play a critical role at the intersection of individual health and public health systems. Early detection allows timely treatment, reduces transmission, and significantly lowers long-term healthcare costs. As diagnostic technologies evolve and access to testing improves, the global market is entering a phase of accelerated innovation and adoption.

Understanding STD Diagnostics: The Backbone of Prevention and Treatment

STD diagnostics refers to a wide range of laboratory and point-of-care tests designed to identify infections transmitted primarily through sexual contact. These tests can analyze blood, urine, or swab samples depending on the suspected infection and testing method.

The primary goal of STD diagnostics is early and accurate detection. Early diagnosis not only improves treatment outcomes but also helps break the chain of transmission within communities. This is especially important because many STDs do not show immediate symptoms, leading individuals to unknowingly spread infections.

Beyond clinical treatment, STD testing is also a cornerstone of preventive healthcare strategies. Routine screening programs for sexually active individuals, pregnant women, and high-risk populations have become standard practice in many countries. Moreover, the rise of point-of-care testing and home self-testing kits is transforming how people access sexual health services, making testing more private, faster, and more convenient.

Key Growth Drivers Shaping the Global STD Diagnostics Market

1. Rising Global Incidence of STDs

One of the strongest drivers behind market growth is the increasing global burden of STDs. According to global health agencies, millions of new infections occur every day worldwide. Rising cases of HIV, syphilis, gonorrhea, and chlamydia, particularly among young adults and high-risk groups, have intensified the need for widespread, reliable diagnostic testing.

Public health campaigns and media awareness initiatives are encouraging more people to get tested, while governments are expanding screening programs. As untreated STDs can lead to serious complications, healthcare systems are placing greater emphasis on early detection, directly boosting demand for diagnostic products and services.

2. Advances in Diagnostic Technologies

Technological innovation is transforming the STD diagnostics landscape. Molecular diagnostics, especially nucleic acid amplification tests (NAATs), have significantly improved sensitivity and specificity compared to traditional methods. These tests allow for faster and more accurate detection, even in early-stage infections.

At the same time, rapid diagnostic tests (RDTs) and point-of-care (POC) platforms are gaining popularity, particularly in primary care settings and resource-limited regions. The growing acceptance of self-testing kits is also reshaping consumer behavior, offering privacy and convenience without compromising reliability.

Automation, digital integration, and even AI-assisted laboratory workflows are further improving efficiency and turnaround times. For instance, in April 2023, Jiangsu Bioperfectus Technologies Co., Ltd. announced CE marking for its Herpes Simplex Virus Type I/II Real-Time PCR Kit, strengthening the trend toward integrated, high-precision diagnostic solutions.

3. Expanding Government and NGO Initiatives

Governments and international organizations such as WHO and UNAIDS are playing a crucial role in expanding access to STD testing. National screening programs, awareness campaigns, and subsidized diagnostic services are increasing testing volumes, especially in developing countries.

A notable example is Canada’s STBBI Action Plan 2024–2030, introduced with new funding to address rising rates of gonorrhea and syphilis. Similar initiatives worldwide are reinforcing the importance of diagnostics in disease control strategies, ensuring sustained growth for the market.

Challenges Limiting Market Potential

Social Stigma and Limited Awareness

Despite technological progress, social stigma remains a major barrier to STD testing in many regions. Fear of judgment, cultural taboos, and lack of education prevent many individuals from seeking timely diagnosis. This leads to underdiagnosis, delayed treatment, and continued transmission.

Overcoming stigma requires long-term investments in public education, community outreach, and confidential testing solutions. Without addressing these social barriers, the full potential of the STD diagnostics market cannot be realized.

High Costs and Limited Access in Low-Income Regions

Advanced diagnostic methods like NAATs offer superior accuracy but are often expensive and infrastructure-dependent. In low- and middle-income countries—where STD prevalence is often highest—limited healthcare infrastructure and financial constraints restrict access to these technologies.

While rapid tests provide a more affordable alternative, they may not always match the sensitivity of laboratory-based methods. Bridging this gap between cost, accessibility, and accuracy remains one of the industry’s biggest challenges.

Market Insights by Test Type and Technology

Chlamydia Testing Diagnostics Market

Chlamydia testing represents one of the fastest-growing segments due to the infection’s high prevalence and often asymptomatic nature. NAATs remain the gold standard, while rapid POC tests are increasingly used in primary care and community clinics. Government screening programs and rising awareness are further accelerating demand.

HIV Testing Diagnostics Market

HIV diagnostics continues to be a cornerstone of the STD testing ecosystem. Rapid tests, self-testing kits, and confirmatory laboratory assays all play vital roles. Global efforts to promote early diagnosis and treatment adherence ensure steady, long-term demand for HIV testing solutions.

STD Molecular Diagnostics Market

Molecular diagnostics dominate the market thanks to their high accuracy, speed, and multiplexing capabilities. These tests are widely used in hospitals and diagnostic laboratories, particularly for chlamydia, gonorrhea, syphilis, and HIV. Although costs remain a concern, ongoing innovation is expected to expand adoption further.

Next-Generation Sequencing (NGS) in STD Diagnostics

NGS is emerging as a powerful tool for comprehensive pathogen detection and drug resistance analysis. While currently limited to advanced laboratories due to cost, declining prices and technological improvements are likely to make NGS a key component of future STD diagnostics, especially in epidemiological surveillance and complex cases.

End-User Landscape: Hospitals, Clinics, and Beyond

Hospitals & Clinics

Hospitals and clinics remain the largest end-user segment, offering everything from rapid tests to advanced molecular diagnostics. They are trusted centers for confirmatory testing, counseling, and integrated treatment services. Even as self-testing grows, clinical settings continue to play a central role in comprehensive STD care.

Regional Market Highlights

United States

The U.S. is one of the largest markets for STD diagnostics, driven by rising infection rates and strong healthcare infrastructure. Widespread use of NAATs, rapid tests, and home-testing kits, supported by public health campaigns and insurance coverage, keeps the market dynamic and innovation-focused.

Germany

Germany benefits from robust healthcare systems, strong public awareness campaigns, and high adoption of advanced laboratory diagnostics. The growing acceptance of self-testing kits among younger populations is also contributing to steady market growth.

India

India’s market is expanding rapidly due to increasing urbanization, rising awareness, and government initiatives such as the National AIDS Control Programme. While affordability and infrastructure remain challenges in rural areas, low-cost rapid tests and private sector participation are driving momentum.

Brazil

Brazil’s market is supported by strong public health programs offering free or subsidized testing, especially for HIV and syphilis. Rapid tests are widely used in public facilities, while private laboratories contribute through advanced molecular diagnostics.

Saudi Arabia

Saudi Arabia’s market is growing steadily under Vision 2030 healthcare reforms. Increased awareness, expanding diagnostic infrastructure, and digital health investments are gradually reducing cultural barriers and improving access to STD testing.

Market Segmentation Overview

By Test Type:

Chlamydia, Gonorrhea, Syphilis, HPV, HSV, HIV, Trichomonas, Mycoplasma genitalium, Chancroid

By Technology:

Immunoassay-based Methods, Molecular Diagnostics, Next-Generation Sequencing, Biosensor/Microfluidics & Emerging Platforms

By Location of Testing:

Central & Hospital Laboratories, Rapid Point-of-Care Platforms, Over-the-Counter/Home Self-Testing

By End User:

Hospitals & Clinics, Diagnostic Laboratories, Home Care/OTC

By Geography:

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Competitive Landscape

The global STD diagnostics market features several major players, each analyzed across five viewpoints: Overview, Key Person, Recent Developments, SWOT Analysis, and Revenue Analysis. Key companies include:

Abbott Laboratories

F. Hoffmann-La Roche AG

Hologic Inc.

Becton, Dickinson and Company

Danaher Corporation (Cepheid)

Siemens Healthineers AG

bioMérieux SA

Thermo Fisher Scientific Inc.

Qiagen N.V.

Bio-Rad Laboratories Inc.

These companies are investing heavily in R&D, automation, and next-generation technologies to strengthen their market positions.

Final Thoughts: Diagnostics as the First Line of Defense

The Global STD Diagnostics Market is entering a decisive decade. With the market projected to grow from US$ 16.82 billion in 2024 to US$ 30.84 billion by 2033, diagnostics is no longer just a supporting function—it is a frontline defense in global public health.

Rising awareness, technological innovation, and strong government initiatives are reshaping how societies detect and manage sexually transmitted diseases. While challenges such as stigma, cost, and access remain, the overall trajectory is clear: faster, more accurate, and more accessible testing will define the future of sexual healthcare.

About the Creator

Sakshi Sharma

Content Writer with 7+ years of experience crafting SEO-driven blogs, web copy & research reports. Skilled in creating engaging, audience-focused content across diverse industries.

Keep reading

More stories from Sakshi Sharma and writers in Trader and other communities.

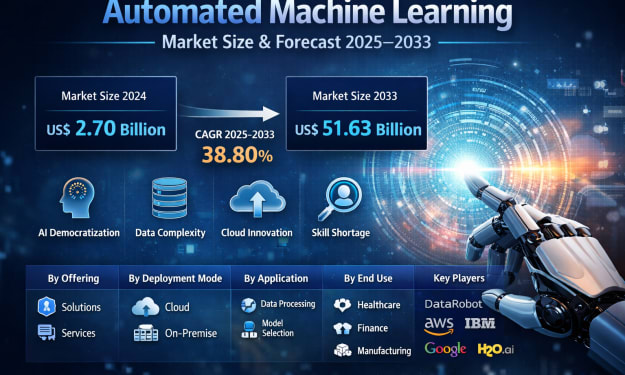

Automated Machine Learning Market Size and Forecast 2025–2033

Introduction: The Rise of Automated Intelligence According to Renub Research’s latest industry outlook, the Automated Machine Learning (AutoML) Market is projected to surge from US$ 2.70 billion in 2024 to US$ 51.63 billion by 2033, expanding at a remarkable CAGR of 38.80% from 2025 to 2033. This extraordinary growth reflects a broader shift in how organizations across the world are adopting artificial intelligence—not as a niche, expert-only capability, but as a mainstream business tool.

By Sakshi Sharmaabout 10 hours ago in Trader

Boeing Stock Analysis: Can Boeing Recover and Regain Investor Confidence?

Introduction Boeing stock has experienced significant volatility over the past few years, making it one of the most debated names in the aerospace and defense sector. As a global leader in aircraft manufacturing and defense technology, Boeing plays a vital role in commercial aviation, military defense, and space exploration. While safety issues, production delays, and financial pressure have challenged the company, investors continue to watch closely for signs of a sustainable turnaround.

By Hammad Nawaz3 days ago in Trader

When Amazon Says You’re a Disappointment

Yesterday, for the first Wednesday in months, I didn’t publish a piece on Vocal. Believe me, I wanted to. I had it all written up and ready to go. I was going to share the news that I had officially become a published author.

By Sandy Gillman2 days ago in Writers

Comments

There are no comments for this story

Be the first to respond and start the conversation.