United Kingdom Diabetes Devices Market Size and Forecast 2026–2034

Rising Diabetes Burden, Digital Health Adoption, and Smart Monitoring Technologies Are Reshaping the UK’s Diabetes Care Landscape

United Kingdom Diabetes Devices Market: An Expanding Healthcare Priority

The United Kingdom diabetes devices market is entering a phase of steady and technology-driven expansion, reflecting both the rising burden of diabetes and the healthcare system’s growing emphasis on early diagnosis, continuous monitoring, and long-term disease management. According to Renub Research, the market is expected to grow from US$ 1,214.80 million in 2025 to US$ 2,333.50 million by 2034, registering a compound annual growth rate (CAGR) of 7.53% from 2026 to 2034.

This growth trajectory is being fueled by several converging factors: the increasing prevalence of both type 1 and type 2 diabetes, the rapid adoption of continuous glucose monitoring (CGM) systems, rising demand for advanced insulin delivery devices, and a broader shift toward digital and connected healthcare solutions. The UK’s healthcare ecosystem, with its strong focus on prevention, patient self-management, and evidence-based care, is creating a favorable environment for the sustained adoption of diabetes devices across hospitals, clinics, pharmacies, and home-care settings.

Understanding Diabetes Care Devices and Their Role

Diabetes care devices are medical technologies designed to help patients monitor blood glucose levels and administer insulin or other therapies to maintain optimal glycemic control. These devices include self-monitoring of blood glucose (SMBG) meters, continuous glucose monitoring systems, insulin pens, insulin pumps, and increasingly, digital platforms and connected applications that track, analyze, and share patient data with healthcare providers.

The core objective of these devices is to empower patients to manage their condition more effectively. Regular monitoring of blood glucose levels enables timely adjustments in diet, physical activity, and medication, thereby reducing the risk of complications such as cardiovascular disease, kidney failure, neuropathy, and vision loss. In recent years, the integration of digital connectivity—such as smartphone apps, cloud-based data storage, and remote monitoring features—has further enhanced the clinical and practical value of these devices.

In the United Kingdom, the acceptance of diabetes devices has increased significantly due to the rising number of diagnosed patients and the healthcare system’s strong emphasis on early intervention and self-care. Improved accessibility, wider reimbursement discussions, and greater awareness of CGM technologies have all contributed to higher adoption rates, particularly among patients who require intensive insulin therapy or close glucose monitoring.

Key Growth Drivers in the UK Diabetes Devices Market

1. Increasing Rates of Diabetes and an Aging Population

One of the most powerful drivers of market growth is the steady rise in diabetes prevalence across the United Kingdom. Lifestyle changes, increasing obesity rates, sedentary behavior, and longer life expectancy have all contributed to a growing pool of patients living with both type 1 and type 2 diabetes. The aging population further intensifies this trend, as older adults are more likely to require regular glucose monitoring and insulin therapy.

Diabetes devices play a crucial role in preventing complications and reducing hospitalizations by enabling consistent, accurate, and timely disease management. As the patient base expands, so does the demand for SMBG devices, CGM systems, and insulin delivery solutions. According to data from diabetes associations in the UK, millions of people are either diagnosed with diabetes or considered at high risk, underscoring the long-term need for reliable and scalable diabetes management tools.

2. Deployment of Advanced Monitoring and Digital Health Solutions

Technological innovation is reshaping the diabetes care landscape in the UK. Continuous glucose monitoring systems, smart insulin pens, and automated insulin delivery devices are becoming increasingly popular due to their ability to provide real-time data, improve treatment accuracy, and reduce the burden of manual monitoring.

These advanced devices not only enhance glycemic control but also improve patient compliance by simplifying daily routines and offering actionable insights. The integration of devices with smartphones and digital health platforms allows patients and clinicians to track trends, identify risks, and adjust treatment plans more efficiently.

In recent years, regulatory and clinical bodies in the UK have also taken steps to encourage the adoption of modern monitoring technologies, particularly for children and patients who require intensive management. This policy and clinical support is accelerating the shift away from traditional finger-prick testing toward more continuous and patient-friendly solutions.

3. Emphasis on Preventive and Managed Care

The UK healthcare system places strong emphasis on preventive care, early diagnosis, and long-term disease management, especially for chronic conditions such as diabetes. Diabetes devices align perfectly with this approach by enabling patients to take an active role in monitoring and controlling their condition.

Educational initiatives, clinical guidelines, and community health programs increasingly encourage the use of monitoring devices to maintain stable blood glucose levels and prevent complications. As self-management becomes a cornerstone of diabetes care, the demand for reliable, easy-to-use, and clinically proven devices continues to rise across the country.

Challenges Facing the UK Diabetes Devices Market

1. Budgetary Constraints and Reimbursement Pressures

Despite their clinical benefits, advanced diabetes devices such as CGM systems and insulin pumps come with higher costs compared to traditional SMBG meters and syringes. In a healthcare environment where cost-effectiveness is a critical consideration, reimbursement decisions can limit patient access to newer technologies.

Healthcare providers and policymakers must balance innovation with affordability, which can slow the adoption of premium devices even when they demonstrate superior outcomes. This creates a challenge for manufacturers seeking to expand the reach of high-end solutions in the UK market.

2. Patient Adoption and Usability Issues

While availability has improved, not all patients find diabetes devices easy or comfortable to use. Some individuals, particularly elderly patients or those less familiar with digital technologies, may perceive these devices as complex, intrusive, or inconvenient.

Usability, comfort, and simplicity remain key factors influencing adoption rates. Manufacturers and healthcare providers must continue to focus on patient-centric design, training, and support to ensure that technological advancements translate into real-world benefits.

Segment-Wise Outlook of the UK Diabetes Devices Market

United Kingdom SMBG Devices Market

The self-monitoring of blood glucose (SMBG) segment represents a well-established and stable part of the UK diabetes care ecosystem. Glucose meters and test strips are widely used by patients with both type 1 and type 2 diabetes, including those managing their condition through lifestyle changes or oral medications.

The key strengths of SMBG devices lie in their cost-effectiveness, simplicity, and ease of use, making them particularly popular among elderly patients and those who prefer straightforward solutions. Although growth in this segment may be slower compared to newer technologies, steady demand ensures its continued relevance in diagnosis and short-term disease management.

United Kingdom CGM Devices Market

The continuous glucose monitoring (CGM) segment is one of the fastest-growing areas within the UK diabetes devices market. CGMs provide real-time glucose readings, trend analysis, and alerts, enabling patients to manage their condition more proactively without frequent finger-prick tests.

These devices are especially valuable for patients with type 1 diabetes and insulin-dependent type 2 diabetes. Smartphone integration and data-sharing features have further improved user engagement and clinical decision-making. With growing acceptance and strong clinical support, CGMs are increasingly becoming a cornerstone of modern diabetes management in the UK.

United Kingdom Insulin Pumps Market

The insulin pumps segment is driven by demand for precise, flexible, and continuous insulin delivery. These devices allow for continuous subcutaneous insulin infusion, offering greater control and convenience compared to multiple daily injections.

Insulin pumps are primarily used by patients requiring intensive insulin therapy, particularly those with type 1 diabetes. Recent innovations, including semi-automated and hybrid closed-loop systems, have significantly improved treatment safety and effectiveness. Although cost remains a barrier for some patients, this segment continues to represent a high-value and clinically important part of the market.

United Kingdom Insulin Pens Market

Insulin pens have gained widespread acceptance in the UK due to their portability, convenience, and dosing accuracy. Compared to traditional syringes, insulin pens are easier to use and more discreet, making them suitable for both newly diagnosed and long-term insulin users.

The introduction of smart insulin pens with dose-tracking features has further enhanced their appeal. Strong physician preference and patient familiarity continue to support steady growth in this segment.

Distribution Channel Insights

Hospital Pharmacies and Diabetes Clinics/Centers

Hospitals and specialized diabetes clinics play a critical role in the prescription and initial adoption of advanced devices such as CGMs and insulin pumps. These settings are also central to patient education, training, and long-term follow-up.

Retail Pharmacies

Retail pharmacies are one of the most important distribution channels for diabetes devices in the UK. They provide easy access to glucose meters, test strips, insulin pens, CGM sensors, and related accessories. Pharmacists also contribute to patient education and adherence, strengthening the overall effectiveness of diabetes management.

Online Pharmacies

Online channels are gradually gaining traction, particularly for repeat purchases of consumables and accessories. Convenience, home delivery, and digital prescription services are supporting the growth of this segment.

Regional and City-Level Market Dynamics

London

London represents the largest and most advanced diabetes devices market in the UK. High population density, strong healthcare infrastructure, and rapid adoption of digital health technologies drive demand for CGMs, insulin pumps, and smart insulin pens. The city’s focus on preventive care and early adoption of innovation further strengthens market growth.

Manchester

The Manchester market benefits from a growing diabetic population and improving healthcare infrastructure. There is strong demand for SMBG devices and insulin pens, with rising interest in CGMs. Community healthcare initiatives and retail pharmacies play a key role in expanding access to diabetes devices.

Leeds

Leeds shows stable growth supported by a well-integrated healthcare system and a strong emphasis on preventive care. While SMBG devices and insulin pens remain dominant, CGM adoption is gradually increasing through specialty care channels.

Liverpool

Liverpool’s diabetes devices market is driven by effective public healthcare services and a focus on chronic disease management. SMBG remains widely used due to affordability, while awareness of CGM systems is steadily increasing through hospital and community programs.

Market Segmentation Overview

By Type:

Self-Monitoring Devices

Continuous Glucose Monitoring Devices

Insulin Pumps

Insulin Pens

By Distribution Channel:

Hospital Pharmacies

Retail Pharmacies

Diabetes Clinics/Centers

Online Pharmacies

Top Cities:

London

Manchester

Birmingham

Leeds

Liverpool

Edinburgh

Glasgow

Tyneside

Bristol

Rest of United Kingdom

Competitive Landscape

Key companies operating in the UK diabetes devices market include:

Abbott Laboratories, Roche, Medtronic, Novo Nordisk A/S, Terumo Corporation, Eli Lilly, BD, and Dexcom Inc.

These companies compete across multiple dimensions, including product innovation, digital integration, clinical performance, distribution reach, and strategic partnerships. Their portfolios typically cover glucose monitoring systems, insulin delivery devices, and supporting digital platforms, with continuous investment in research and development to improve patient outcomes.

Final Thoughts

The United Kingdom diabetes devices market is on a clear growth path, supported by rising disease prevalence, technological innovation, and a healthcare system that increasingly prioritizes prevention and self-management. With the market projected to grow from US$ 1,214.80 million in 2025 to US$ 2,333.50 million by 2034 at a CAGR of 7.53%, the sector offers strong opportunities for device manufacturers, healthcare providers, and digital health innovators alike.

While challenges related to cost, reimbursement, and usability remain, the long-term outlook is positive. As digital health integration deepens and patient-centric care models continue to evolve, diabetes devices will play an even more central role in improving quality of life and clinical outcomes for millions of people across the United Kingdom.

About the Creator

Sakshi Sharma

Content Writer with 7+ years of experience crafting SEO-driven blogs, web copy & research reports. Skilled in creating engaging, audience-focused content across diverse industries.

Keep reading

More stories from Sakshi Sharma and writers in Trader and other communities.

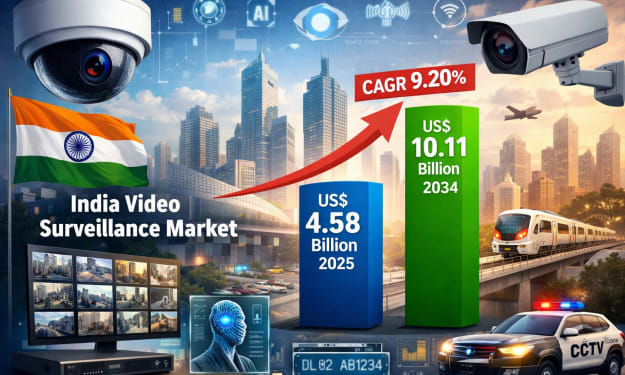

India Video Surveillance Market Size and Forecast 2026–2034

Introduction India’s rapid urbanization, digital transformation, and growing focus on public safety are redefining how security is planned and implemented across the country. One of the most visible outcomes of this shift is the accelerated adoption of video surveillance technologies across public, commercial, residential, and defense sectors. According to Renub Research, the India Video Surveillance Market is expected to grow from US$ 4.58 Billion in 2025 to US$ 10.11 Billion by 2034, registering a strong CAGR of 9.20% during the period 2026–2034.

By Sakshi Sharmaa day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.