Europe STD Diagnostics Market Size and Forecast 2026–2034

How Technology, Policy, and Preventive Care Are Redefining Sexual Health Diagnostics Across Europe

Introduction

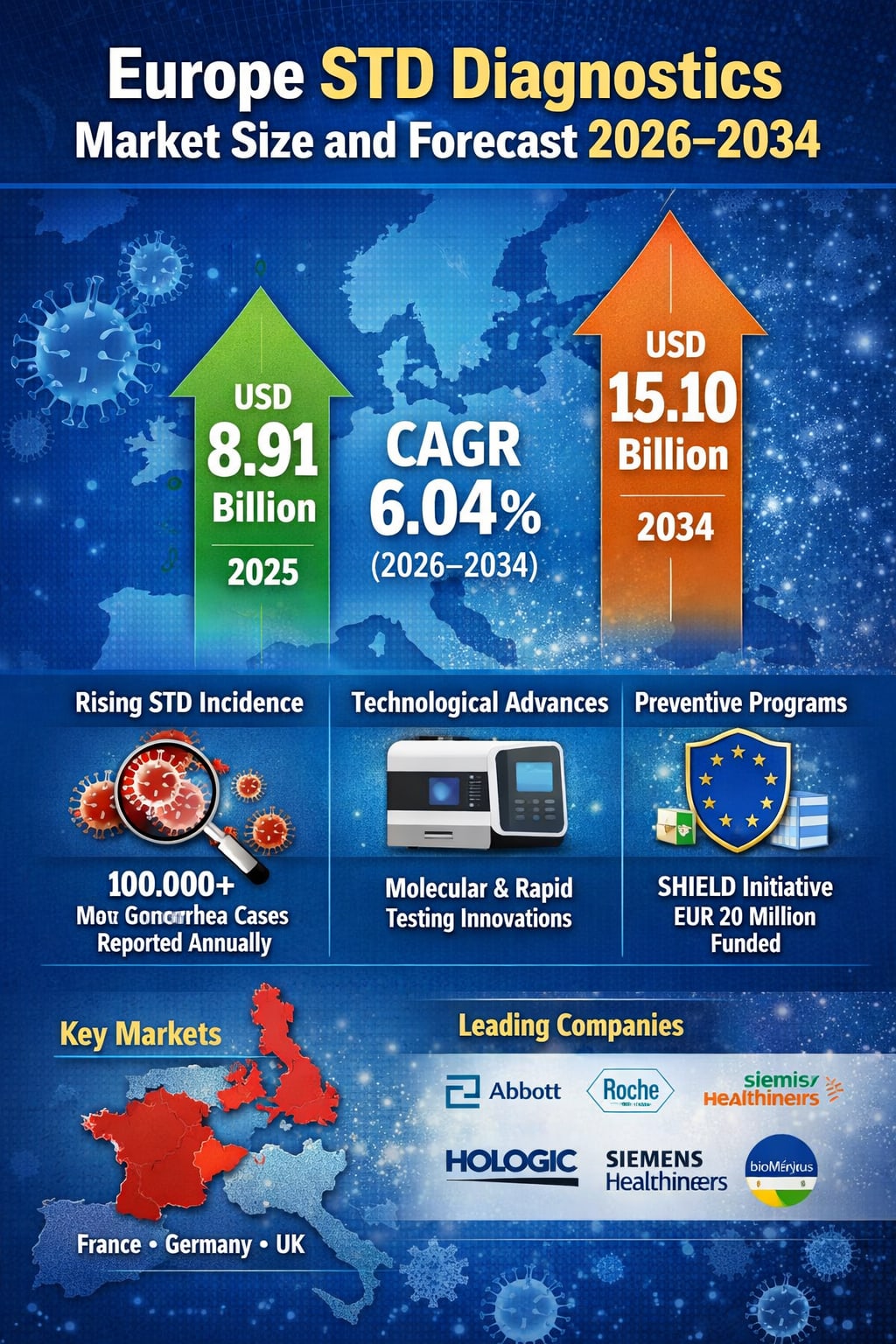

The Europe sexually transmitted disease (STD) diagnostics market is entering a phase of sustained and meaningful expansion, driven by rising disease prevalence, stronger public health surveillance, and rapid advances in diagnostic technology. According to Renub Research, the Europe STD diagnostics market is projected to grow from USD 8.91 billion in 2025 to USD 15.10 billion by 2034, registering a compound annual growth rate (CAGR) of 6.04% during 2026–2034.

This steady growth reflects not only increasing testing volumes but also a broader shift in how Europe approaches sexual health—moving toward early detection, decentralized testing, and stigma-free access. With robust healthcare infrastructure, strong regulatory oversight, and expanding preventive programs, Europe continues to position STD diagnostics as a core pillar of public health policy.

Understanding STD Diagnostics

STD diagnostics refer to laboratory and point-of-care tests used to detect infections such as chlamydia, gonorrhea, syphilis, HIV, HPV, HSV, trichomoniasis, and mycoplasma genitalium. These diagnostics include serological tests, molecular methods such as polymerase chain reaction (PCR), rapid antigen and antibody tests, and emerging self-testing solutions.

The primary objective of STD diagnostics is early and accurate identification of infections to enable timely treatment, prevent complications, and reduce onward transmission. In Europe, routine screening of pregnant women, sexually active youth, and high-risk populations has become an integral component of healthcare delivery.

Growing Importance of STD Diagnostics in Europe

Europe’s increasing STD burden and heightened focus on healthcare monitoring have significantly boosted diagnostic demand. Public health authorities actively encourage regular screening among vulnerable populations, while education campaigns have helped reduce stigma around testing.

The region’s advanced healthcare ecosystem supports the rapid adoption of molecular diagnostics, multiplex testing, and automated laboratory platforms. Confidential testing services, faster turnaround times, and greater test accuracy have further strengthened public confidence, driving higher utilization across both urban and rural areas.

Key Market Drivers

Rising Burden of Sexually Transmitted Diseases

The increasing incidence of STDs remains the most powerful growth driver for the European diagnostics market. Infections such as chlamydia, gonorrhea, syphilis, and HIV continue to rise, prompting stronger surveillance and expanded screening initiatives.

Data from the European Centre for Disease Prevention and Control shows that nearly 100,000 new gonorrhea cases were reported recently—more than four times higher than a decade ago. This alarming trend has reinforced the urgency for early, frequent, and accessible testing across the region.

Technological Advancements in Diagnostic Solutions

Innovation in diagnostic technologies is transforming STD testing across Europe. Molecular diagnostics now offer superior sensitivity and specificity, enabling accurate detection even in asymptomatic cases. Automation and digital integration have improved laboratory efficiency, while multiplex testing allows simultaneous detection of multiple pathogens from a single sample.

In December 2025, F. Hoffmann-La Roche AG received CE Mark approval for its cobas BV/CV assay, capable of accurately identifying bacterial and yeast infections using vaginal samples. Such developments underscore the rapid pace of innovation shaping the European STD diagnostics landscape.

Expansion of Screening and Preventive Healthcare Programs

Government-supported screening and preventive initiatives play a crucial role in market expansion. One notable program is SHIELD Joint Action, funded with nearly EUR 20 million under the EU4Health initiative, involving 25 EU Member States through 2028.

The program aims to prevent infections linked to cancer—such as HPV, hepatitis B/C, and HIV—by simplifying access to vaccination, testing, and treatment. These initiatives significantly increase testing volumes while reinforcing long-term public health outcomes.

Market Challenges

Fragmented Healthcare Systems

Europe’s fragmented healthcare landscape presents a structural challenge. Diagnostic approvals, reimbursement policies, and procurement processes vary widely across countries. A test approved in France may face delays or cost barriers in the UK or Eastern Europe, complicating market entry strategies for diagnostic companies.

Barriers for Small Diagnostic Companies

Smaller diagnostic firms often struggle to navigate Europe’s complex regulatory and reimbursement frameworks. Limited financial resources and varying national standards make large-scale expansion difficult, often favoring established multinational players.

Persistent Stigma and Limited Patient Engagement

Despite increased awareness, social stigma surrounding STDs continues to hinder testing uptake, particularly in conservative regions. Fear of embarrassment or discrimination reduces participation in screening programs, affecting overall market growth. While self-testing and point-of-care solutions help mitigate this challenge, cultural barriers remain.

Segment Analysis

Europe Syphilis Testing Market

The syphilis testing segment is witnessing renewed growth due to rising infection rates and the serious risks associated with untreated disease. Antenatal screening and blood donor testing remain central, supported by laboratory-based serological assays and confirmatory algorithms. Rapid tests are increasingly used in outreach and mobile health programs.

Europe HIV Testing Market

Europe’s HIV testing market is mature yet steadily expanding. Laboratory immunoassays remain dominant, but rapid and self-testing solutions are gaining traction due to convenience and privacy. Early diagnosis and prompt linkage to care continue to drive innovation and decentralized testing models.

Europe STD Molecular Diagnostics Market

Molecular diagnostics represent the fastest-growing and highest-value segment of the market. Widely used for chlamydia and gonorrhea detection, these tests offer unmatched accuracy and scalability. Although capital-intensive, molecular platforms dominate centralized laboratories and large hospital systems across Europe.

Europe STD Rapid Point-of-Care Platform Market

Rapid point-of-care diagnostics are gaining popularity for their ability to deliver same-visit results and treatment. These platforms are particularly valuable in STD clinics, emergency settings, and mobile testing programs. Ongoing improvements in accuracy are accelerating adoption despite cost considerations.

Hospitals and Clinics: The Largest End-User Segment

Hospitals and clinics account for the largest share of the Europe STD diagnostics market. Hospitals rely on high-throughput analyzers for complex cases, while clinics prioritize rapid diagnostics to support efficient patient flow. Integration with electronic medical record (EMR) systems is increasingly influencing purchasing decisions.

Country-Level Insights

France

France benefits from a strong, government-supported healthcare system with extensive national screening programs. In July 2025, France launched Europe’s first free, home-order self-collection program for chlamydia and gonorrhea testing among women aged 18–25, further expanding diagnostic access.

Germany

Germany represents one of Europe’s most technologically advanced STD diagnostics markets, supported by high healthcare spending and robust laboratory infrastructure. Private and hospital laboratories drive adoption of automated molecular platforms, emphasizing prevention and patient dignity in testing experiences.

United Kingdom

The UK STD diagnostics market is closely aligned with public health objectives focused on early detection and prevention. Sexual health clinics and screening centers sustain high testing volumes, while innovation in molecular and point-of-care diagnostics supports steady market growth despite budgetary constraints.

Russia

Russia’s STD diagnostics market shows significant regional variation. While major cities possess advanced laboratory capabilities, rural areas rely on simplified testing methods. Public health campaigns and demand for cost-effective diagnostics present long-term growth opportunities.

Market Segmentation Overview

By Test Type:

Chlamydia, Gonorrhea, Syphilis, HPV, HSV, HIV, Trichomonas, Mycoplasma Genitalium, Chancroid

By Technology:

Immunoassays, Molecular Diagnostics, Next-Generation Sequencing, Biosensors & Microfluidics

By Location of Testing:

Central & Hospital Laboratories, Rapid Point-of-Care, Home Self-Testing

By End User:

Hospitals & Clinics, Diagnostic Laboratories, Home Care / OTC

By Country:

France, Germany, Italy, Spain, UK, Belgium, Netherlands, Russia, Poland, Greece, Norway, Romania, Portugal, Rest of Europe

Competitive Landscape

The Europe STD diagnostics market is led by global diagnostic giants with strong R&D capabilities and extensive distribution networks. Key players include:

Abbott Laboratories

Hologic Inc.

Becton Dickinson and Company

Danaher Corporation

Siemens Healthineers AG

bioMérieux SA

Thermo Fisher Scientific Inc.

Qiagen N.V.

Bio-Rad Laboratories Inc.

Each company has been analyzed across five viewpoints: overview, key personnel, recent developments, SWOT analysis, and revenue performance.

Final Thoughts

The Europe STD diagnostics market is on a clear upward trajectory, supported by rising disease prevalence, policy-driven screening initiatives, and continuous technological innovation. As healthcare systems increasingly prioritize early detection, decentralized testing, and patient-centric care, diagnostics will remain central to Europe’s public health strategy.

With strong backing from governments, healthcare institutions, and industry leaders, the market’s growth from USD 8.91 billion in 2025 to USD 15.10 billion by 2034 highlights a future defined by accessibility, accuracy, and prevention-focused healthcare delivery.

About the Creator

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts26 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.