Understanding the Bank of England Base Rate: What It Means for You and the Economy

How the central bank’s key decision shapes loans, mortgages, savings, and the cost of living across the UK

When the Bank of England (BoE) announces a change in its base rate, headlines fill the news, financial experts start debating, and households across the UK wonder what it means for them. But beyond the numbers and jargon, the base rate plays a huge role in shaping the economy—from how much you pay on your mortgage to the interest you earn on your savings.

Understanding the Bank of England’s base rate isn’t just for economists or investors; it affects everyone’s daily life. Let’s explore what it is, why it matters, and how its changes ripple through the economy.

---

What Is the Bank of England Base Rate?

The base rate is the official interest rate set by the Bank of England’s Monetary Policy Committee (MPC). It represents the cost of borrowing money for commercial banks and influences almost every other interest rate in the economy.

When the BoE raises the base rate, borrowing becomes more expensive. That means higher mortgage rates, more costly loans, and often better returns for savers. On the other hand, when it lowers the rate, borrowing becomes cheaper, encouraging spending and investment but reducing savings returns.

In simple terms, the base rate acts as a financial steering wheel, helping the Bank of England control inflation and keep the economy stable.

---

Why the Base Rate Matters

The Bank of England’s main job is to keep inflation around 2%, ensuring prices rise at a steady and manageable pace. When inflation gets too high—like it has in recent years—the BoE raises the base rate to slow down spending and cool the economy.

Conversely, when inflation is too low or the economy is struggling, the bank cuts rates to make borrowing easier and boost growth.

This careful balancing act aims to keep the economy from overheating or slipping into recession. But for ordinary people, these changes have very real effects:

Mortgage holders face higher or lower monthly payments depending on rate changes.

Savers might see their bank interest rates rise or fall.

Businesses find it easier or harder to borrow money for expansion.

Consumers experience changes in the prices of goods, services, and credit.

In short, the base rate is one of the most powerful tools in managing the UK economy.

---

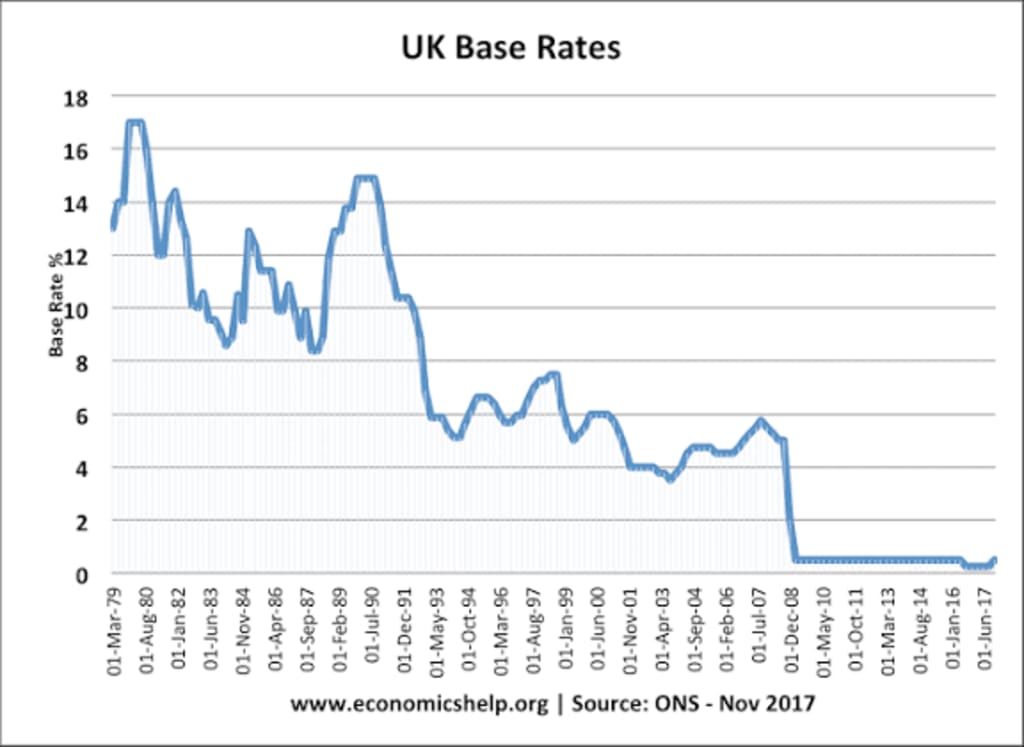

A Look at Recent Trends

Over the past few years, the Bank of England’s base rate has been on a rollercoaster ride. During the COVID-19 pandemic, the rate was slashed to a historic low of 0.1% to support the economy. But as inflation surged due to supply chain disruptions, energy crises, and global conflicts, the Bank began steadily increasing the rate.

By mid-2023, the base rate climbed above 5%, marking its highest level in over a decade. This rapid rise aimed to bring down inflation, which had reached more than double the target rate.

For homeowners with variable-rate mortgages, this meant a significant increase in monthly payments. For savers, it brought better returns—but often not enough to fully offset inflation’s impact.

---

How the Base Rate Affects You

Whether you’re a homeowner, renter, saver, or business owner, changes to the base rate affect you directly or indirectly.

Homeowners: If you have a variable or tracker mortgage, your monthly payments rise when the base rate goes up. Those with fixed-rate deals won’t feel the impact until their term ends.

Renters: Landlords facing higher mortgage costs may raise rents to cover their expenses.

Savers: Higher base rates generally mean better savings account interest—but inflation can still erode purchasing power.

Borrowers: Personal loans, car finance, and credit cards may all become more expensive as rates increase.

Businesses: Small and medium-sized firms may delay investments if borrowing costs rise too quickly.

Essentially, when the base rate moves, it shifts the balance between spending and saving across the economy.

---

What’s Next for the Bank of England Base Rate?

As of late 2025, the big question remains: Will the Bank of England start cutting rates again?

Economists are divided. Some believe that as inflation slows and the economy cools, the BoE may begin to ease rates to encourage growth. Others warn that cutting too soon could reignite inflation.

The Monetary Policy Committee reviews the rate roughly every six weeks, examining factors like employment, GDP growth, and consumer prices before making a decision. Each announcement draws attention because it signals the Bank’s confidence—or concern—about the UK’s economic health.

---

How to Prepare for Future Changes

You can’t control what the Bank of England decides, but you can plan ahead:

If you have a mortgage, consider locking into a fixed rate before any further increases.

If you’re saving, look for accounts offering the best interest or consider longer-term savings products.

If you run a business, manage debt carefully and prepare for possible fluctuations in borrowing costs.

Stay informed about MPC meetings and decisions—they can affect your finances faster than you might expect.

---

The Bottom Line

The Bank of England base rate is more than a number announced every few weeks—it’s a signal of where the economy is heading. Each change reflects how the Bank views inflation, growth, and financial stability in the UK.

Whether you’re paying off a mortgage, saving for the future, or running a small business, understanding the base rate helps you make smarter financial choices.

In an unpredictable economy, one thing remains constant: the base rate is the heartbeat of Britain’s financial system, and keeping an eye on it can make all the difference between financial strain and smart planning.

About the Creator

Fiaz Ahmed

I am Fiaz Ahmed. I am a passionate writer. I love covering trending topics and breaking news. With a sharp eye for what’s happening around the world, and crafts timely and engaging stories that keep readers informed and updated.

Keep reading

More stories from Fiaz Ahmed and writers in The Swamp and other communities.

Zelenskyy Calls for Ukraine to Join EU Before 2030 After Commission Delivers Warning on Corruption – Europe Live

In a bold and emotional appeal, Ukrainian President Volodymyr Zelenskyy has called for his country to be accepted into the European Union before 2030, even as the European Commission released a report highlighting ongoing concerns over corruption and governance. The speech marks another crucial moment in Ukraine’s ongoing effort to align itself with Europe — politically, economically, and morally — amid the backdrop of its war with Russia.

By Fiaz Ahmed 4 months ago in The Swamp

Why Black History Matters in America?

The United States of America is celebrating their 250th anniversary in 2026. I'm proud to be an American and as someone who was born here, I wouldn't imagine myself living anywhere else. This is a country where opportunities are possible. Where anyone can be successful in anything they desire to do. Equality, community, and togetherness are the backbones of what America is and should be about. However, we have an administration who wants to erase and disregard those who have made positive, meaningful impacts in our country, specifically Black figures, such as Martin Luther King, Jr., Rosa Parks, and Maya Angelou. President Trump and his administration have been constantly complaining and fighting against what they call the "Woke agenda". They use this excuse as a distraction from other issues they refuse to address, such as the high cost of living, climate change, and inflation. That equality is dividing America, when in reality, it's bringing us together. Being woke is not tied to a specific political party. No matter where you stand on the political spectrum, you can still care about other people and their plights. Compassion and empathy for others isn't tied to a political party, either. We were taught as children to treat others the way we want to be treated and not judge others because they're different from us. Caring about others isn't a personal attack on your beliefs. It doesn't make you any less of a person. People who are easily offended over African American figures, past or present, or anything related to it, are grasping at straws. Current and future generations need to know who people like Harriet Tubman and Shirley Chisholm were, especially in the classroom. Black History is part of American History. It should be recognized, not hidden or forgotten. Besides, you can't shield children from everything, just because your feelings are easily hurt.

By Mark Wesley Pritchard 18 days ago in The Swamp

Rhode Island Shooting: Grief, Fear, and Community Response

The words rhode island shooting carry a weight that is hard to explain unless you have felt it in your own neighborhood. A shooting does not only affect the people directly involved. It ripples through schools, homes, workplaces, and quiet streets that once felt safe. Parents hold their children a little tighter. Neighbors glance at each other with questions in their eyes. Fear settles in slowly, like a fog that refuses to lift.

By Muqadas khan3 days ago in The Swamp

The Tango Connection

I suppose I've become a writer so I wouldn't bore everyone to death telling them my stories. Reading them is reading. Not the same. There's rhythm. And timing and, most importantly, drama and suspense. Unless you have tremendous magnetism and an undeniable stage presence, there's no way you can engage an audience the way you can by writing your story. That's my opinion.

By Rene Volpi 6 days ago in Beat

Comments

There are no comments for this story

Be the first to respond and start the conversation.